Brightwork Research Study: 3rd Party SAP and Oracle Support

Executive Summary

- The 3rd party support category for SAP and Oracle is an important and growing area for customers of these vendors.

- This research study covers the background on 3rd party support and the major providers.

The Study

This is our study into the current state of 3rd party SAP and Oracle support.

Introduction

There is sparse information published in the area of software called 3rd party support. A primary reason for this is that all of the IT analysts are aligned with vendors — and software vendors do not want their customers to consider using 3rd party support. One of the exceptions to this was the 2019 first time publication of Gartner’s Market Guide for Independent Third-Party Maintenance for IBM, Oracle, and SAP Software. This was in our view, one of Gartner’s better reports, however, it presented the move to 3rd party support as a primary cost-driven affair, and what was left out entirely was the estimation of the support quality provided by SAP and Oracle. This demonstrates either Gartner’s compliance to these mega-vendors or their pattern of only speaking to senior members of the software buyers — individuals who have no experience opening tickets or dealing with SAP or Oracle support. Something else important left out is what support for most SAP and Oracle customers actually is — or how it is consumed.

What is SAP and Oracle Support in its Consumption?

There is roughly speaking a lifecycle to support.

As time goes by after an SAP or Oracle purchase and after the implementation, there usually is a period where tickets are opened and closed. In this stage, the customer has hopes and the customer is led to believe that many of their requirements can and should be met by standard SAP and Oracle functionality. This process is also described by the following quotation.

In addition, software OEMs typically increase software support and maintenance costs each year. However, support requirements will often decline for an enterprise as internal technical expertise grows and the application’s stability matures, thereby widening the gap between software support cost and its realized benefits.

Many enterprises have not only paid software fees for licenses they are not using (shelfware), but also continue to pay 20–22 percent annual maintenance on them. – Beroe

Through the process, the employees within the customer are gradually worn down and desire to open fewer and fewer tickets.

Through this entire process, SAP and Oracle support personnel is trained to never admit any shortcomings of the SAP applications or to contradict anything stated by SAP sales during the sales process.

The eventual desirable state is for these vendors to have almost no tickets opened up, and for the customers to continue to pay support, but for the support offered to be as close to minimal as possible. In the case of SAP, they have a variety of areas that aren’t covered the standard 22% of list price standard support. And furthermore, SAP has an exorbitant support offering called MaxAttention that is really more like consulting. SAP points customers out to MaxAttention when they can’t get their needs met by standard support. All of this makes a mockery of the presentation of support capabilities made by both vendors during the sales phase. SAP and Oracle support is essentially free money for both of these vendors.

In a number of clients we have consulting with, they opened a very minor number of support tickets, and the support being paid to SAP or Oracle would have to be classified as a “security blanket.” There are assertions to the contrary, such as this quote from ComputerWeekly.

That’s because CIOs and businesses around the world are taking control of their IT systems, and are unwilling to pay high maintenance prices anymore.

However, this is an odd statement as there are few 3rd party support providers and very few of any size. The vast majority of SAP and Oracle customers use the standard support provided by these vendors. And the following quotation from ComputerWeekly..

Increased interest in Rimini Street’s services and support indicates a significant shift in the market away from ERP vendors to third party providers.

..does not change this. Rimini Street and the entire 3rd party support company’s business would have to explode for a “significant shift” in the market away from ERP vendors to third party providers to occur. (and this quote is from January of 2017, so back when 3rd party support was less common than it is in 2020.)

Rather, the increase in interest in Rimini Street is an indication of the support being almost entirely with SAP and Oracle to other providers.

Why Did Gartner Leave Out the Margin on SAP and Oracle Support?

The margin obtained by support, which is well known to be in the 90% range from SAP and Oracle financial reports, is never mentioned once in Gartner’s report on 3rd party support.

Why?

Also, how did SAP and Oracle obtain this margin — or more specifically how did SAP and Oracle cut the costs of their support, while increasing its costs to obtain this margin?

The 3rd party support vendors don’t appear afraid to call this out.

Alongside this push to the cloud, Oracle and SAP have modified the structure of their support models. Whereas customers once paid maintenance fees to get more personalized support, in-version product enhancements, and the right to new upgrades, they now pay fees for self-support tools, fewer to no enhancements, and the right to repurchase cloud-based replacement solutions. They have become de-personalized support, but many customers remain on board, paying more each contract and viewing downgraded support through a lens of “business as usual.” – Spinnaker Support

Everything in the quotation above, we have witnessed first hand. Did Gartner neglect to bring this up because it would have caused an uproar from SAP and Oracle that are major funders of Gartner?

It appears quite likely that this is the case.

This is because you have to make a concerted effort to write a seventeen-page analysis of 3rd party support and leave out this topic from the paper.

What Do SAP and Oracle Support Cover?

Something entirely left out of the report by Gartner was what do SAP and Oracle cover versus 3rd party support providers. It is curious that Gartner would leave this out because all of the 3rd party providers cover far more than either SAP or Oracle. And each of the major 3rd party support providers has a matrix on their websites that show how much more they offer than SAP or Oracle.

Therefore even the price reduction illustrated by Gartner in their quotation understates the direct cost savings.

The average annual savings is at least 50% when comparing TPSM services costs to the annual maintenance pricing models and policies of IBM, Oracle, and SAP.

In their documentation, Spinnaker Support uses the term “hard savings.”

Most essential to you, the IT leader, is to understand the cost model of third-party support. It brings immediate “hard” savings of about 60% compared to software vendor-provided maintenance fees.

However, we prefer the term direct. The other savings from 3rd party support are also hard and quantifiable, but they are not immediately from the time of switching to 3rd party support.

Due to the vast difference in what 3rd party support providers cover versus SAP or Oracle, the quote above from Gartner is not at all fully explanatory of the situation. As 3rd party support providers cover so much more, and other areas of the report do not elaborate on the distinctions.

Gartner is not alone in condensing the difference between vendor support and 3rd party support as being primarily about cost as the following quotation from ComputerWeekly illustrates.

By using a third-party maintenance provider, businesses can manage their costs and reinvest their savings in those areas of business that are of strategic importance.

And their report also does not explain the differences in responsiveness.

With SAP and Oracle support, tickets must be opened, and the responsiveness to the tickets is low. These vendors use tactics to delay the solving of issues. They are not available by phone, and they do not engage in screen shares. Their strategy is to put as much bureaucracy between the customer and their support. Third-party support providers are far more available and responsive.

Naturally, the margins of the 3rd party support providers are considerably lower than SAP or Oracle as not only do they charge much less, but their costs are far higher as they cover so much more, and what they do cover, they cover more extensively.

Direct Support Costs or Total Support Costs?

Another topic ignored by Gartner is the total cost reduction. Gartner, once again chooses to discuss the direct costs. These are the money paid for support to SAP or Oracle versus the money paid to 3rd party support providers. However, as Rimini Street has done a very good job illuminating, the direct costs are only the tip of the iceberg.

The iceberg construct is probably the best known in the 3rd party support field. It explains that the costs saved go far beyond just the direct costs paid to the support provider.

The Predominant 3rd Party Vendor Support

Something to note is that the three largest 3rd party support entities all are larger in Oracle support than SAP support. Roughly speaking, the three largest 3rd party support entities average around thirty percent of their business coming from Oracle support, with 30% or less coming from SAP.

What Supported Products?

Third party support entities are all significantly smaller than the support organizations of each of the vendors. Although, as previously mentioned, most 3rd party support entities cover each application much more in-depth than the SAP or Oracle. However, the vendors certainly win in breath. Both SAP and Oracle have an enormous number of products, and 3rd party support entities cannot support every product that SAP or Oracle offers. However, each vendor tends to have its sales concentrated in a small percentage of its overall product database.

This table lists the products that each 3rd party entity states that they support.

Oracle has often explained as a software company that is consistently a single company, but in fact, Oracle is two companies.

- Oracle as a Database Company: One is a database company where the majority of the databases it has sold are over the needs of the buyers (that is some of the database functionality of Oracle is necessary, but only for a minority of the licenses that are purchased).

Oracle as an Application Company: The second is essentially a Computer Associates model for its applications.

Oracle’s model is based upon control which is enabled through a combination of Oracle’s well-respected database, along with an enormous number of acquired applications.

Oracle has more than 340 products which are the most of any software vendor. Much like other mega software vendors ranging from SAP to Salesforce to IBM, Oracle does not so much develop new products as it simply acquires them.

Why Isn’t Oracle A Story of Three Companies?

When Oracle acquired Sun Microsystems, they acquired Sun’s hardware business. This business had been in decline for years as commodity hardware had been putting pressure on Sun’s server business. Larry Ellison thought that the trick would be to combine Sun’s hardware with Oracle software into “appliances.” The premier example of this being Oracle Exadata, which is a server purpose-built to run the Oracle database. However, we don’t consider Oracle’s hardware division to be the third leg of Oracle, because Oracle’s hardware strategy has failed. Every year, Oracle’s hardware division declines and their hardware becomes increasingly niche, and this looks to only continue. Our view is that Oracle’s hardware division is a distraction for Oracle, and this is supported by the revenues of Oracle’s hardware division.

The dual nature of Oracle is expressed in how development occurs differently with its database from its applications.

- Oracle’s Database Development: Oracle is well known for the talent in its database development group. Oracle is constantly pushing innovation in its database and every new version tends to include capabilities that other databases do not have. As we will discuss, Oracle’s RDBMS database is running out of areas it can develop where it does not add unnecessary complexity to the database and compete with functionalities that are for instance better managed in other software categories, virtualization (VMware) being a prominent example.

- Oracle’s Application Development: Unlike Oracle’s database, Oracle’s applications are entirely acquired. After an application is acquired by Oracle, there is a predictable loss of talent within the acquired vendors after they transition to becoming Oracle employees. This is particularly true among the most central employees to each of the vendors. This leakage of central employees is credited as a reason why Oracle’s applications do not tend to progress very much after they are acquired. This is sometimes referred to as the Computer Associates (CA) model.

In fact, outside of its database, Oracle has had demonstrated a great difficulty in developing either new applications or further significantly developing applications that it acquires. Large software vendors run into diseconomies of scale in managing large software portfolios. The advantage to size is found in the marketing and account control of these vendors.

In each case, Oracle combines account control with the strategy of pushing the broadest number of software products into their enormous customer base.

- Gaining Database Growth: When Oracle acquires an application, it begins to sell it into its account base, but more than this, Oracle requires an Oracle database license to be sold with the application. Customers can use a different database other than Oracle, but they still need to pay for the Oracle license. As a consequence, this naturally drives Oracle database sales. In effect, Oracle takes away the database choice from customers when they acquire an application.

- Comprehensive Software BOMs: By owning so many applications, Oracle can sell very large BOMs to companies, and this allows it to discount some products in the BOM when facing off against a point solution. Even when that point solution is preferred by the business, Oracle’s pricing flexibility can make the acquisition of a point solution look like an extravagance.

Oracle’s application acquisition strategy is designed to give it more account control over its customers and allows it to defend almost any software category against another vendor. This is a very effective short to medium term strategy but runs into complications due to the longer term limitations in forward development of the acquired Oracle applications.

Undeclared Realities Around the Oracle’s Database

The Oracle database is well known as the core of Oracle’s business and what has allowed Oracle the cash flow to both make their large number of acquisitions as well as provided them with their account control.

- Oracle quite frequently makes inaccurate assertions around the Oracle database to customers, IT analysts, IT media entities, and to investors.

- We will fact check Oracle’s assertions and what it means for Oracle’s longer-term business model and Oracle customers.

What About SAP Aligned Support?

SAP aligned support is when normally a consulting company provides support along with SAP. This is a way for SAP to “distribute some revenues” to their ecosystem. SAP runs a large system of patronage where for instance consulting firms are given consulting business in return for recommending SAP. SAP also has a number of connection firms that receive preferential treatment by SAP.

SAP alighted support is normally a step down even from SAP support, or where SAP provides all of the support. Most of what occurs is the consulting firm provides management of tickets, with the majority of the technical answers coming from SAP.

The following is a very common type of quotes around the cloud from Oracle.

“Some of the biggest stars are Oracle’s Autonomous Database, its Fusion ERP and human capital management cloud applications, and its NetSuite cloud application suite. Shrinking businesses include some on-premise hardware products.

You have these very modern businesses…growing very rapidly, taking share, clear #1s in the overall marketplace,” Ellison said. “And you have these other businesses that are melting away, and we just don’t care.

For example, for its 2019 fiscal year ended May 31, Oracle’s Fusion ERP and HCM cloud applications revenues grew 32%, and its NetSuite revenue grew 32%.” – Forbes

Very little of this quotation is true.

We already addressed the Autonomous Database in the database section. Let us address the other areas discussed in the quote.

Is Netsuite Driving Oracle Growth?

Oracle has reported fast growth with NetSuite, and this may be true, but NetSuite is less than 1/40th of Oracle’s overall revenue, and it is a lower priced item and has a far lower margin than Oracle’s other products. That is, its growth is not particularly impactful on Oracle’s income statement. Vendors often tout their cloud business, but what is as frequently left out is that the cloud business tends to be low margin.

Is Fusion ERP and HCM Cloud Driving Oracle Growth?

The statement around Fusion ERP and HCM Cloud growth is quite false.

For years now Oracle has played an accounting trick by selling customers both the on-premises applications and then the duplicate cloud-based application. However while the customer implements the on-premises version, the sales rep is compensated on the basis of the cloud license, and the cloud license sale is reported to Wall Street as a cloud sale. This information comes from multiple Oracle sales rep and is a well known “secret” within the company. Because of this, it is highly unlikely and unknowable (from the outside) how much Fusion ERP or HCM Cloud grew. It cannot be discerned from reviewing Oracle’s financial statement. As has been the case since Oracle semi-duplicated its on-premises applications to SaaS version (the Fusion project), Oracle customers have not migrated to these SaaS versions. This is explained by a Rimini Street survey.

“This makes sense in light of the fact that migration to Oracle SaaS requires a full “rip and replace” for the modules impacted, essentially making it a reimplementation. In addition, Oracle has stated that its own Soar cloud migration ERP program does not apply to 93% of their installed base. Cost issues also factor into customer decisions, with 30% finding Oracle’s offering too expensive. Even Oracle CEO Mark Hurd has stated in investor calls that customers who move to Oracle’s SaaS will typically pay three times more than they pay before doing so. “

Oracle as On Premises First

Oracle continues to be predominantly an on-premises software vendor. The vast majority of its database and application business continues to be delivered on premises. Oracle is posing as a cloud company because this is the storyline that Wall Street has told Oracle they want to hear, allowing them to obtain the maximum valuation.

Although we are straightforward in observing that Oracle is misleading Wall Street, this section was not written to critique Oracle or to say that because Oracle is predominantly not cloud that this reduces their prospects. The most profitable software vendors continue to be on premises, not cloud vendors.

Fake It Until You Make It (to the Cloud)?

Oracle is not a cloud vendor, and it does not have a pathway to becoming a cloud vendor. Oracle is a cloud vendor to Wall Street and on-premises vendor to its customers.

Oracle is continually trying to connect up items that are not related to the cloud to the cloud. The following are prominent examples of Oracle’s messaging.

Oracle's Cloud Information

| Information Communicated by Oracle | Description |

|---|---|

| Oracle's Autonomous Database is Inherently Related to the Cloud? | Oracle tries to connect the Autonomous Database to the cloud, which while necessary to be from the cloud, (because it is not actually autonomous), but it is not actually otherwise related to the cloud. |

| Oracle's Applications are Increasingly Delivered by the Cloud | Oracle has been pitching the migration from on premises applications to cloud for over a decade and still, very few of the Fusion based applications are in use. |

| Oracle is Driven by Cloud Revenues? | Oracle tries to connect its revenues to the cloud, which are not related to the cloud. |

Oracle figured out what Wall Street wanted to hear, and manufactured that story. Oracle’s strategy has been to do as little internal adjustment as possible while posing as cloud to the outside world. The following comment is consistent with the position that Oracle takes.

Oracle Cloud is Growing?

“Catz then brought up the company’s recent cloud partnership with Microsoft—a blockbuster agreement that I analyzed recently in Microsoft-Oracle Shocker: Customers Win as #1 and #6 Vendors Pair Up—and predicted it would become another growth engine for not only the new self-driving database but also the Oracle Cloud overall.

“In addition, the recent interconnect agreement with Microsoft will only help accelerate the transition from on premise database to the Autonomous Database service,” Catz said.”

The Oracle Cloud is not growing in usage. In fact, its usage is so low that it is normally not measured by those entities that measure usage. This is because it is below 1% of the overall market for cloud services. The numbers some IT media entities report that is higher than this are self-reported by Oracle. This seems to have no bearing on the reporting of the overall cloud services market.

Oracle has been making claims around the growth of Oracle Cloud for years now. If the growth story is occurring, why has the Oracle Cloud not passed 1% of the total cloud services market? Continual rapid growth, without being, is not a logical possibility. Over the past 10 years, if you had cancer in your body that was growing at the rate of the Oracle Cloud, you would be fine.

Secondly, if Oracle Cloud is growing, why is Oracle partnering with Microsoft and their Azure cloud service offering? The reason is that Oracle is not investing much in its cloud data centers. Oracle prefers to redirect funds that could go to data center investment to stock buybacks. Oracle’s investment in its cloud data centers has been extremely small. Investment in infrastructure has too long of payback horizon for Oracle.

Oracle’s Cloud Pitch Versus Customer Buy-In

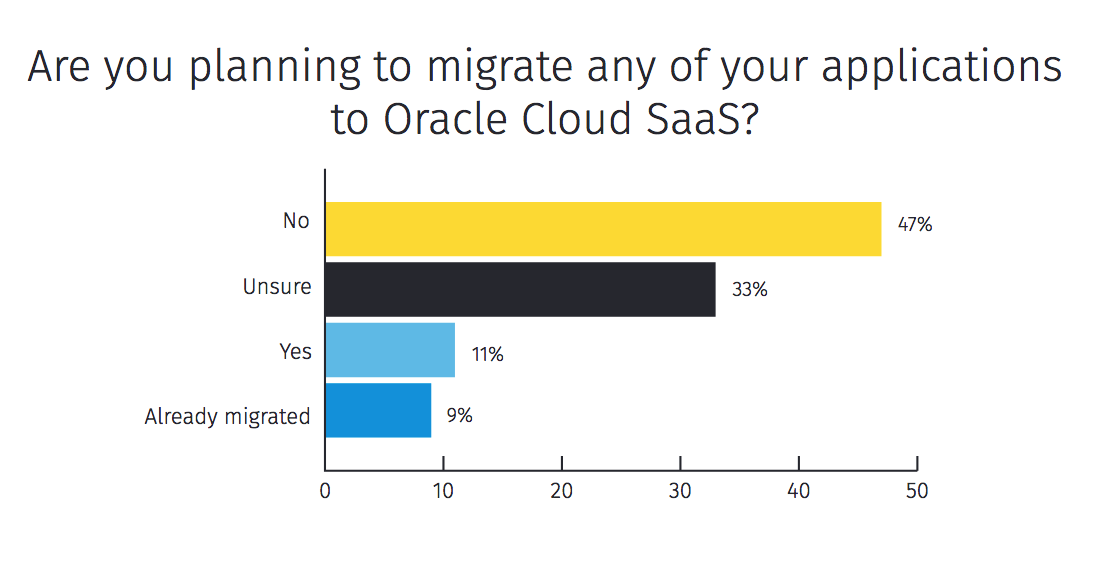

Rimini Street observes the following around what Oracle tells customers versus the plans customers have to move to the Oracle Cloud.

“The main strategy presented by Oracle today is to move to the Oracle Cloud, particularly Oracle Cloud SaaS applications. The vendor claims it will reduce costs and simplify ongoing maintenance and support. However, the majority of respondents plan have not or do not plan to migrate to Oracle Cloud SaaS applications (see chart in Takeaway #4), but 26% of respondents have already chosen to lift and shift their Oracle applications to a cloud-hosted environment.”

The graphic above is from Rimini Street. It shows exactly what we see on Oracle accounts, a very different story than presented by Oracle on customer plans to move to Oracle Cloud.

What About Separate Support from SAP Aligned Entities?

This following quotation is from an article by Forrester.

..it makes sense to ask the larger systems integrators, such as Wipro, Tata Consultancy Services, IBM Global Services, and Siemens (SIS), which are also the largest SAP integrators, to quote for offering SAP third-party maintenance. These integrators naturally don’t make a lot of noise about these things, as they also have a partner relationship with SAP, of course. At the end of the day, the demand will be balanced with the supply — and if more customers request SAP maintenance from their systems integrator, they will start to offer it. – Martin Schindler

There are a number of inconsistencies here — and each partner values its consulting business far more than its support business. Providing 3rd party support creates a wedge between the consulting firm and SAP.

The quote continues.

A large systems integrator like Wipro, for example provides significant support for client-specific developments (custom applications). In the framework of large-scale outsourcing deals, banks, telecom companies, and airlines already receive maintenance services for custom-built applications. Having once understood the delivery of maintenance, it is less effort to expand it to SAP applications. With deal volumes above $250 million, you can set up a team of at least 20 people who only take care of the bugs in the application logic. – Martin Schindler

This is an interesting proposal, but we have not seen this.

That is not to say that consulting firms do not do what Martin Schindler has stated, but we question a few aspects of this explanation. This is expressed by the following quotation.

All SAP partners are also system integration experts. When they take projects directly or via SAP, the scope generally includes non-SAP systems. They do not go and say we will customize SAP to make it work for you but if customers ask for it, they do it.

We pause here in the quote. This is because most of the customization performed by consulting firms in both SAP and Oracle projects is unanticipated. Recall that customers are informed that the applications they are buying contain best practices, which is a construct used to both diminish the customer’s pre-existing applications and to have the customer underestimate the custom development that will occur during and implementation as we cover in the article When Should a Company Use ERP Best Practices Versus Custom Code, and in the article How SAP Uses Best Practices to Control the Implementation.

Let us resume with the quote.

The typical billing rates for offshore development and SI work is between $35 to 50 an hour. A few resources are billed up to 100$ per hour. For example ABAP Developments are billed between $25 to 40 per hour with a few topping 60 depending on clients demand for various expertise levels. In the US the comparable billing rates are 3x to 5x. Someone like me will be billed at 1000 to 2000$/day. depending on the employer. When SAP does the implementations, they hire consultants from the market but they have a lot of utilities of their own that they do not share with their partners.

In SAP IS projects 20 to 30% customization is not unheard of. When clients demand it, SAP does it too. Their best practice lectures are primarily for less demanding customers. – Loknath Rao (Longtime APO consultant)

Therefore, “3rd party support” is really just an extension of these consulting firm’s work. They in many cases pick up “3rd party support” business as an extension of the consulting project — particularly as it becomes increasingly apparent that the customer requires long term custom code support — that of course they thought was going to be handled by SAP functionality. There is also a strategy used by consulting firms to specifically not document, so as to lengthen the consulting contract or obtain the support contract.

This is a common trick. Support projects after implementation and then more support. If you do not document or document it poorly they come back to you. SAP doesn’t even document standard fields. Then they say its documented on help.com Loknath Rao

This leads into an important topic related to the independence of support and support entity from SAP.

The Inconsistency of 3rd Party Support when an Entity is an SAP Partner

The following quotation comes from the Savantis website.

As an SAP gold partner, Savantis focuses on helping SAP customers manage and make the most of their SAP investments. Our support services can help you channelize the time, effort and money in innovative programs that enable agility and drive growth.

This is a certification badge that is meant to encourage customers to use Savantis. However, in reality, it is a major disadvantage and should even be considered disqualifying.

Here is why.

Any entity with a certification badge from SAP or Oracle has no independence from SAP or Oracle. And sure enough, we found false information on the Savantis website regarding SAP. SAP and Oracle partners are required to promote SAP or Oracle. And this is the exact last thing a customer wants in support. SAP or Oracle can call up any of these entities during a new sales pursuit, and have the support manipulated to push for whatever SAP or Oracle wants to sell.

There is a secondary question, which also applies to any company seeking to provide “3rd party support” that is aligned with SAP or Oracle. And that is what percentage of support SAP receives. As SAP or Oracle will often expect a cut — this makes the costs higher. Even if a company were not a partner with SAP or Oracle in their support side, but were a partner through their consulting arm, SAP or Oracle could easily pressure the company through the consulting side — and the consulting side is far higher in revenue than the support business.

Therefore, we do not consider the support that is aligned or provided by entities that are partners with SAP or Oracle to be 3rd party support. By our definition, 3rd party support must be non-aligned support. We consider SAP or Oracle support provided by companies that are partners with SAP to be “SAP remotely controlled support.”

Oracle’s growth outside of acquisitions has been tepid for several years.

A limiting factor on future Oracle growth is the Oracle software position of customers after years of some of the most aggressive sales quotas set in the enterprise software space and the implication on the applications and databases that are already sold into the Oracle account base. The following table is just a few examples of techniques used by Oracle to meet previous quarters.

Previous Oracle Sales Tactics

| Oracle Sales Tactic | Description |

|---|---|

| Forced Purchases | Through various pressure tactics (including audits and breach of notices) Oracle frequently forces customers into purchasing items that both Oracle and the customer know that the customer will not use. These items are normally cloud related and are driven by Oracle's need to show cloud "growth" to Wall Street. |

| Breach of Notice | This gives the customer a legal letter which stipulates they either stop using Oracle software in 30 days or come to the table to negotiate more purchases. A breach of notice means that Oracle will be negotiating with this customer particularly aggressively. |

| Aggressive Audits | Of all of the software vendors we track, Oracle brings the most aggressive audits against its customers. Most Oracle customers will be audited at least once and often twice in a five year period. |

Unreturned Calls from Oracle Sales Reps?

This has caused many contacts within Oracle customers to “hide” from Oracle account reps. This has led some Oracle sales reps to declare to customers that they have been found to have been possibly in “non-compliance,” flagged for an audit, even when the customer has not, in order to get their customers to respond to them.

Symptoms of Oracle Being Oversold Into Accounts

| Symptom | Description |

|---|---|

| The Growing Separation Between Oracle and their Customers | Oracle's sales goals and their customers are far apart. |

| Dealing With Previous Oracle Investments | Long term Oracle customers are still confused about unlocking existing Oracle investments. |

| Sales Goals | Oracle sales leadership is pushing Oracle Cloud, Oracle cloud versions of on-premises applications. |

| Information from Oracle Sales | Reports from many Oracle sales reps is that their accounts are oversold. |

Oracle Reps Pitching the Comprehensive Cloud Stack Story

Oracle sales reps have to approach these frustrated customers with so-called comprehensive cloud stack story. Oracle offers every cloud need that a customer would ever have. This is not considered a sellable story (see our section on Oracle Cloud).

We have tested Oracle Cloud and would never use Oracle Cloud nor recommend Oracle Cloud regardless of the free trials Oracle offers or the cloud credits that Oracle offers.

The Future Sales Opportunities at Oracle Accounts

Overall, Oracle sales reps face an uphill battle in meeting their sales quotas, which explains the aggressive behind the scenes pressure tactics to make targets.

- This places a strong limiting cap on Oracles growth potential, particularly considering that Oracle, once the marketing hyperbole is stripped away, Oracle not offering very much new to its customer base.

- In this way, it faces similar sales limitations to SAP. That is, these are two vendors that have already “stuffed” their accounts, and that has already sold into most of the accounts that they are able to sell into. However, this is not the story Oracle is obviously telling the outside world. Oracle is pitching itself as a future growth story. A company with a better cloud than AWS. A company with a database that is gaining, not losing market share.

Conclusion

Oracle’s public presentation bears little correspondence to how Oracle functions in reality. Oracle has taken to promoting itself entirely based upon what the investment community wants to hear.

Oracle Synopsis

| Oracle Postion | Description |

|---|---|

| The Reality Around the Oracle Cloud | Oracle will move to copy SAP's strategy of not investing in cloud but using its account control to markup the cloud services of other cloud service providers. This is what the Oracle/Microsoft Azure partnership is about. However, given the fact that a public cloud is price published and therefore transparent, it is unlikely that Oracle will be allowed to continually markup Azure to customers. |

| Oracle Support | We are not the first to refer to Oracle's support revenue as the Golden Goose. Oracle has optimized its support not to support customers but to attain an extremely high margin. Oracle will continue to lose support revenue to third-party support providers at an increasing rate. Oracle's lawsuits against third-party support providers like Rimini Street have essentially failed, and Oracle is vulnerable to losing more support business in the future and its margin. |

| Oracle and Database Hosting | Oracle will continue to lose on-premises database hosting to AWS. When this occurs, the account control at the migrating customer declines, and there is the likelihood of Oracle resources being shed from the customers. The Oracle resources are the main "lobby group" within companies to continue to invest in Oracle. |

| Oracle Database Marketshare Erosion | Open source databases and less expensive commercial databases like Microsoft SQL Server will continue to reduce the market share of the Oracle database. |

| Pressure on Oracle's Margin | Most of Oracle's margin is in its support which will increasingly see pressure as Oracle's database is increasingly understood as less differentiated. Oracle has reached the end of its ability to differentiate its database by adding more functionality or further growing the scope of the Oracle database. The fact that such a small percentage of Oracle customers are on recent versions of the Oracle database is clear evidence that Oracle customers do not see the new functionality of the Oracle database as worth either the expense or the extra software bloat. |

Oracle makes many aggressive proposals around its growth story. However, none of these stories are legitimate. On the contrary, Oracle is more likely to see its revenues decline (in place of more acquisitions, and therefore more financial leverage).

The Problem with Oracle’s Broader Value Proposition

This is another graphic from Rimini Street’s poll of customers.

Oracle’s substantial lock-in is preventing its revenues from eroding more than they ordinarily would. For example, I was recently advising a company that spent $4 million per year on support but was scared away from using a third party support alternative. Even though they barely used Oracle support because they had roughly 10% of their Oracle databases that that to be supported by Oracle. This meant the other 90% of their databases could not be removed from Oracle support (in the client’s mind). They did not like the value they were getting support, and they did not like Oracle, but they renewed their support because they felt they had to. This scenario is repeated over and over with customers paying Oracle not because they want to, but because of the lock-in that Oracle has over them.

These lock-in strategies are keeping Oracle’s revenues afloat. However, this is not a situation that can be considered a growth scenario.

References

Just because article links are included below, does not mean they are endorsed.

https://www.gartner.com/en/documents/3957130/market-guide-for-independent-third-party-maintenance-for

*https://www.techcompanynews.com/spinnaker-support-fastest-growing-third-party-support-managed-services-company-world/

*https://go.forrester.com/blogs/10-03-16-sap_3rd_party_maintenance_an_alternative_for_me_part_two/

https://www.beroeinc.com/blog/third-party-software-maintenance-support-pros-cons/

https://www2.computerworld.com.au/brand-post/content/611167/demand-for-3rd-party-erp-support-soars/

https://www.vertexone.net/services/sap-support

*https://spinnakersupport.com/faq/

*https://spinnakersupport.com/blog/2016/08/03/7-reasons-consider-third-party-sap-software-support/

*https://spinnakersupport.com/download/what-it-leaders-need-to-know-white-paper.pdf

*https://sap.cioreview.com/cxoinsight/is-thirdparty-sap-software-support-right-for-your-organization-nid-6072-cid-49.html

*https://cio.sia-partners.com/overview-third-party-maintenance-alternative

https://www.gartner.com/doc/reprints?id=1-1YYS9WXZ&ct=200505&st=sb

https://www.computerweekly.com/news/252470433/Why-it-makes-sense-to-use-third-party-to-keep-the-IT-lights-on

*https://www.panorama-consulting.com/shifting-erp-system-maintenance-to-a-third-party-support-provider/

*https://www.forbes.com/sites/oracle/2019/02/05/5-reasons-rimini-street-other-lower-cost-software-maintenance-providers-may-be-more-expensive/#60be03e65511

This is a paid placement by an Oracle “contributor” to Forbes, which is just an article designed to get companies to not use 3rd party support. There is no declaration anywhere that the article was funded by Oracle.

https://cdn2.hubspot.net/hub/109944/file-16326017-pdf/docs/forrester_third-party-software-support-marketplace-qanda_-_copy.pdf

https://www.computerworld.com/article/3418336/sap-ceo–not-concerned–with-rise-of-third-party-maintenance-and-support-players.html

https://diginomica.com/jones-packaging-rewraps-sap-erp-rimini-street

A curious article with virtually no analysis — published back when Diginomica received funding from SAP.

https://www.constellationr.com/research/positive-pricing-impact-third-party-maintenance-oracle-and-sap-customers

*https://earlyadopter.com/2018/05/22/how-third-party-support-is-evolving-to-add-value-and-new-services/

*https://blog.softwareinsider.org/2010/02/22/mondays-musings-why-users-must-preserve-their-third-party-maintenance-rights/

https://dealarchitect.typepad.com/files/cowensoftware09252009.pdf

https://www.forbes.com/sites/danwoods/2016/04/18/why-third-party-software-support-is-possible-and-a-good-idea/#5300cb906c77

https://www.cio.com/article/3025465/logistics-company-saves-big-by-ditching-oracle-support.html

https://www.networkworld.com/article/2298429/the-pros-and-cons-of-third-party-software-support.html

https://www.infoworld.com/article/2628482/is-it-time-to-switch-to-third-party-software-support-.html

https://www.riministreet.com/Documents/Collateral/Rimini-Street-Research-Report-Lower-Cost-and-Risk-for-SAP-on-Journey-to-Cloud.pdf