The 2021 US Real State Bubble

Executive Summary

- In June of 2021, there are multiple financial bubbles that require analysis in the US.

Introduction

This article covers 2021 US real estate bubble and will propose an investment strategy based upon this analysis.

Bubble #1 Real Estate Bubble

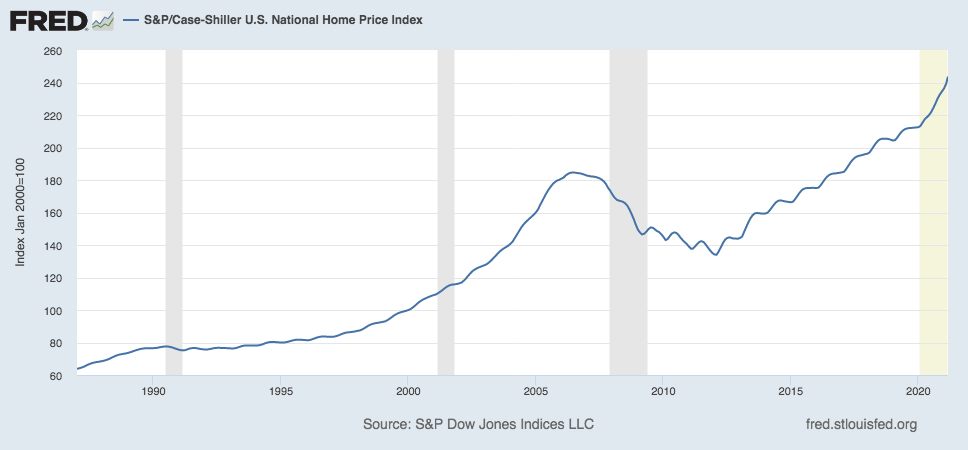

How Much is the Housing Market Overheated By the Last Bubble?

At the peak of the 2006 and the 2021 real estate bubble the Case Schiller index was the following over the trough of the period that preceded it.

- The peak to trough from 2000 to 2006 is 185%

- The peak to trough from 2012 to 2021 is 183%

Furthermore, the Case-Schiller index is released quarterly.

Each bubble was driven by different factors. The 2006 bubble was driven by very lax lending standards and subprime mortgages. The 2021 bubble has been driven by extremely low-interest rates.

This can be seen in the following graphic.

This was driven as a policy by the Fed to boost the economy, but yet again ended up primarily boosting asset prices. Since 2012 wages are flat or declining, but housing prices are up over 83 percent according to the Case Schiller Index. The peak to trough is nine years instead of six years this time.

This interest rate, dropping to 2.65% in Jan of 2021, on the 30-year mortgage is unprecedented in history going back to 1971. This would seem to indicate that the 30-year mortgage rate will need to rise (and it already has). As this occurs the housing market will cool.

This graph shows the very clear relationship between the 30-year mortgage rate and (contractor/private owner) new housing starts. This correlation (I was unable to download the data set) is extremely high. This means that the Fed’s 30-year mortgage is the determining factor in predicting housing prices and housing bubbles.

How Much As the Bubble Gone Up During the Pandemic?

This is explained as follows.

Even before the pandemic pushed the U.S. housing market into overdrive, the price of the average American home was on a rocket ride, climbing more than 50% between 2012 and 2019. It was the third biggest housing boom in American history. Then came the pandemic, marked by a buying frenzy and a selling freeze, which created a supply-demand mismatch that made the price boom go into warp speed. The average price of American homes, in real terms, is now the highest it’s ever been — even higher than the peak of the housing bubble in 2006 before it crashed 60% and bottomed out in 2012.

Non Bank Lenders More Active Than Ever

Even before the pandemic pushed the U.S. housing market into overdrive, the price of the average American home was on a rocket ride, climbing more than 50% between 2012 and 2019. It was the third biggest housing boom in American history. Then came the pandemic, marked by a buying frenzy and a selling freeze, which created a supply-demand mismatch that made the price boom go into warp speed. The average price of American homes, in real terms, is now the highest it’s ever been — even higher than the peak of the housing bubble in 2006 before it crashed 60% and bottomed out in 2012.

https://readwrite.com/2021/05/07/the-real-estate-market-crash-is-coming-sooner-than-you-think/

This is further explained in the following quotation, which illuminates the shadow banking sector.

Finally, shadow banking, or lenders that don’t take deposits and aren’t subject to regulatory oversight, are responsible for over 50 percent of the home and personal loan market in the United States. Fintech firms are a major part of this lending boom, representing over a quarter of loan origination in 2015, while offering significantly higher rates than traditional banks and other shadow banking firms. And the lending gets even more dangerous when cryptocurrencies, famously volatile, are the medium of exchange. While still nascent, this development in fintech activity will soon merit firm and appropriate regulatory responses from the CFPB, the SEC, and other relevant actors.

*https://cepr.net/robinhood-is-a-perfect-example-of-fintechs-insidious-power/

Shadow Banking

Shadow banking is described in the following quotation.

Shadow Banks Insured by the Fed?

The trade-off, McCulley noted, is that since “they fly below the radar of traditional bank regulation, these levered-up intermediaries operate in the shadows without backstopping from the Federal Reserve’s discount lending window or access to FDIC [Federal Deposit Insurance Corporation] deposit insurance.” That is to say: The one thing that defines their existence is that the government doesn’t guarantee their business. But, just like the bailout of the shadow bank American Insurance Group in 2008, recent events have made a mockery of this idea. Even before mortgage servicers came looking for a handout in April, the Federal Reserve agreed to protect exchange-traded funds, repurchase agreements, and money market accounts, which are the main financing avenues for many shadow bank entities, such as asset managers.

https://newrepublic.com/article/157455/shadow-banks-back-still-big-fail

That is an amazing statement. It means that the Fed is protecting speculative assets, not just bank accounts.

The Lack of Regulation of Shadow Banking

It’s important to understand why conventional banks undergo the strict regulation that shadow banks profit from avoiding. Banks are subject to charters, licensing, and regulation in order to prevent what was a common occurrence in the nineteenth century: bank runs. Rumors and panics, both real and imagined, could spur customers to pull their deposits, which could ruin banks’ livelihoods and bring commercial activity to a standstill. Long recessions and depressions were common. Banking, without a government guarantee, is a volatile business. – New Republic

Yes, banking cannot exist without government support, as we cover in the article The Requirement for Government in Banking.

Was Fannie Mae the First Shadow Bank?

In 1968, the government privatized the Federal Nation Mortgage Association, better known by its nickname, Fannie Mae.

Fannie Mae was, in some ways, a proto–shadow bank, and it issued some of the first mortgage-backed securities. These financial products were an innovative way to privately fund home loans without deposits, and they inspired the emergence of similar tools. One such product was the money market account, introduced in 1971, which was similar to a bank account but classified as an investment. These allowed financial businesses an alternative way to raise money for lending, without the traditional regulation associated with banking. To many customers, money market accounts seemed to function a lot like normal bank accounts. But whether they knew it or not, their money-market deposits, unlike their standard bank deposits, weren’t insured by the government. As alternative schemes of funding proliferated, so did shadow banking in general. – New Republic

Shadow Banks Metastesize and AIG is a Shadow Bank

Hedge funds and other types of investment banks started to dominate the landscape. AIG, which had grown to become a gigantic shadow bank, had—unbeknownst to many—recklessly agreed to be the counterparty to a bevy of credit default swaps, against which it held little capital. When things went south, the government had to stabilize the financial world by accepting the responsibility for all of AIG’s reckless lending—essentially assuming the role of the FDIC for a financial entity that taxpayers were never meant to backstop. In the aftermath of the financial crash, it was revealed that there were a number of grotesquely large shadow banks just like AIG, such as Metlife, Prudential, and GE Capital. – New Republic

- Mortgage Backed Securities (MBSs): A security made up of a bundle or group of mortgages.

- Credit Default Swaps/Obligations (CDOs): An unregulated insurance derivative that is used to insure MBSs.

- Collateralized Loan Obligations (CLOs): This could be anything, but is again a derivative who’s value is based upon some type of asset.

Call them repos, or MBSs, or CLOs they are where an asset of often questionable quality, and unregulated in nature is used to create a loan. In every case when banking is performed without government oversight, a bailout is around the corner. This happened with MBSs and CDOs, it happened with wildcat banking after the banking was decentralized to the states which did not regulate banking, it happened in the S&L crisis. The repo market and growth of shadow banking appear to be the same thing as before, only bigger. This is also covered in a comment on the WP same article.

The first time an unregulated banking sector collapsed the US economy was in 1819, and it became an almost clockwork 20 year cycle after that until the Great Depression, only interrupted by wars that flooded markets with borrowed government money.

In each of these cycles, a few gained tremendously while the many lost their collective shirts, even while we were on the gold standard.

After each of these cycles, the “experts” declared that the underlying causes had been corrected, and a recurrence was unlikely or impossible. Each time they were grossly mistaken, because Greed never goes away, and will always find a new way to feed itself.

Considering a Typical MBS

The following describes a typical MBS.

The Federal Reserve has committed to using every tool in its toolbelt in order to support the economy in its recovery from COVID-19. One of the strategies the Fed has undertaken involves buying $40 million worth of mortgage-backed securities (MBS) per month. Specifically, the Fed is buying what are known as agency MBS. A hypothetical MBS might contain loans from Freddie Mac with borrowers who have 680+ median FICO® Scores and made 20% down payments for 1-unit primary homes. It’s not uncommon for a single MBS to contain 1,000 loans or more.

One of the goals of the Fed is to support consumer borrowing and the free flow of credit in the economy with the goal of supporting the post-pandemic recovery. To that end, the Federal Reserve has been buying a ton of agency MBS. Agency MBS are mortgage-backed securities issued by the government-sponsored enterprises Freddie Mac and Fannie Mae, or the U.S. government agency Ginnie Mae in order to keep mortgage rates low and homeownership accessible. As the largest buyer and holder of agency MBS, the Fed is able to keep its thumb on mortgage rates. We’ll get into the mechanics of why later on, but at a high-level, because the Fed has inflated demand for agency MBS, mortgage rates are kept low. Because the Federal Reserve is buying billions in mortgage bonds every month, this raises demand in the agency MBS market. In turn, yields on those bonds can be lower and still attract a buyer, which has a direct effect leading to lower rates.

https://www.rocketmortgage.com/learn/agency-mbs

So an MBS might have 1000 mortgages contained within them. The Fed is actively purchasing MBSs, which is curious because this is what Freddie Mac and Fanny Mae were designed to do. This is yet another example of the Fed proliferating its role in the economy and exceeding its mandate.

Banks Are Now Lending to Shadow Banks??

In a curious development, shadow banks are now taking over the role of banks. And banks are lending to them.

And even though traditional banks may be making fewer loans to midsize businesses, they’ve been eagerly lending to the hedge funds, private equity firms and business development companies that are making more of those loans. In fact, the fastest growing category of revenue and profit for the banks in recent years has been lending to “non-bank financial institutions.” – WP

This reinforces that banks are getting out of “old fashioned banking” and lending to much larger entities.

However, this means that shadow banks are accessing government-created money, but do not have the regulation of banks. This is yet another abdication of responsibility on the part of banks who have over the decades continually moved further and further away from having any public service function. It makes little sense to charter banks so they can make loans to shadow banks, hedge funds, etc that have zero public service function.

The problem is explained in the following quotation.

Excellent analysis and all true, in my opinion. However, the cure is not necessarily all about regulation. As you describe, the banks are much more regulated but they now participate in this bubble indirectly by lending it to “blackbox” intermediaries instead of directly. Capital will always find ways to find demand. The key is to let these institutions fail miserably when the music stops instead of bailing them out again and again. Most of Wall Street came out much richer than before after 2008 crisis. Not only did they do well, but the FED with its zero interest rate policy and massive purchases of securities made “free” money available for 10 years to these institutions. By keeping the interest rates at zero, the FED also forced the Pension Funds and Endowments into riskier financings with no real oversight. No wonder we keep on running into bubbles and the American savers pay the price. – Comment on Same WP Article

Credit Expansion or Bubble

Middle-market lending, of course, is just part of the biggest expansion in corporate borrowing the U.S. economy has ever seen, a result of eight years of cheap and easy money engineered by the Fed and other central banks after the 2008 financial crisis. Companies have used much of this newly borrowed money to buy back their own shares, pay special dividends to private equity investors and acquire other companies, all of which have the effect of inflating stock prices. – WP

The Shadow Banks Increasingly Push for Insurance from the Fed

The Federal Reserve has already bailed out huge asset managers and other shadow banks by backstopping money market funds, repurchase agreements, and other corporate financing tools. Hedge funds—which, by the way, are supposed to make money in a downturn—are turning to government loans. Venture capital and private equity firms are asking for help, too. It’s likely that more shadow banks will pile on, each with a story of need—and a warning of the consequences to the larger economy if aid isn’t duly rendered.

How the Fed Keeps Expanding its Role and Liabilities

We have moved from a time where deposits were insured, to where the Fed, which has enlarged its role to be the insurer of all private banking interests, is enormously exceeding its mandate and ensuring the entire system (of elite interests) while at the same time fighting against any regulation.

This means that even more strange things are occurring as shadow banking is backed by repos (short-term loans on collateral), which are not regulated.

This secondly means that with an increasingly unregulated lending arena, it is likely there is again fraud. However, as is usually the case, we will only find out about the fraud after the fact. And when these assets depreciate, the Fed will be there to insure them.

The following article is from May of 2019, which means the shadow bank credit bubble was building over two years ago and has been continuing to build.

The Shadow Banks Credit Bubble

Federal Reserve Chair Jerome Powell gave a speech a couple of weeks back that showed that financial regulators have learned many lessons from the 2008 financial crisis, but not the most important one, namely: If regulators wait to act until they can say with certainty that a credit bubble is about to burst, they’ve waited too long.

These shadow banks have made borrowed money cheaper and easier to get, but they have also made the financial system and the U.S. economy more susceptible to booms and busts.

When the Shadow Banks Moved into Mortgages and Consumer Loans

Then, beginning in the 1990s, shadow banks moved aggressively into home mortgages and other consumer debt — auto loans, student loans, credit card debt — which they bought from banks and other lenders, packaged together and sold to investors as bond-like securities. You know how that turned out. – WP

Housing Sales Fall to Low

The following quotes describe the housing status as of late July 2021.

Sales of newly built homes dropped in June to the lowest level since the early days of the coronavirus pandemic in April 2020, according to data released by the U.S. Census Bureau on Monday.

Sales of new single family homes fell to an annualized rate of 676,000, 6.6% below May’s rate of 724,000 and 19.4% below the June 2020 level of 839,000. Analysts were expecting new home sales to increase by 3.4% in June.

After a year of frenzied buying and price gains in the double digits, newly built homes are now out of reach for much of the demand that remains in the market.

The median price of a newly built home in June rose just 6% from June 2020, and while that is a large gain historically, it is nothing compared with the 15%-20% annual gains seen in previous months.

Buyers in June were also hit with higher mortgage rates, which spiked about a quarter of a percentage point during the month. While that may not sound like a lot, if buyers are already stretched by higher home prices, they have less of a financial cushion to absorb higher mortgage rates.

https://www.cnbc.com/2021/07/26/housing-boom-is-over-as-new-home-sales-fall-to-pandemic-low.html

Strategy: Short Housing

How to Short the US Housing Market

Proshares Inverse

“This short ProShares ETF seeks a return that is -2x the return of its underlying benchmark (target) for a single day, as measured from one NAV calculation to the next. Due to the compounding of daily returns, holding periods of greater than one day can result in returns that are significantly different than the target return and ProShares’ returns over periods other than one day will likely differ in amount and possibly direction from the target return for the same period. These effects may be more pronounced in funds with larger or inverse multiples and in funds with volatile benchmarks. Investors should monitor their holdings as frequently as daily. Investors should consult the prospectus for further details on the calculation of the returns and the risks associated with investing in this product.”