The Hindenburg Research Short Stocks

Executive Summary

- Hindenburg Research has multiple reports on stocks that they short.

- We cover some of them in this article.

Introduction

Hindenburg Research shorts many stocks. They do some of the most thorough research into companies that they short.

Ormat (Geothermal)

Founded in 1965, Ormat has grown to one of the largest global producers of geothermal power plants. Geothermal power uses natural heat from the Earth’s core to generate steam to make electricity, fitting well into the “Environmental” part of the ESG narrative. The process is widely considered to be more environmentally-friendly than conventional fossil fuel sources.

The result is that Ormat appears to be plundering the nations it claims to be helping. Kenya’s state power company, for example, is on the brink of insolvency, in significant part due to its overpriced deals with Ormat. A large portion of Honduras’ crippling national debt originates from its inflated private energy deals, such as its deal with Ormat, which virtually guarantees a loss for the state.

Ormat’s counterparties have consistently expressed a desire to renegotiate or terminate its burdensome contracts. We think the consequences of our findings could result in backlash in the countries Ormat does business, along with exposure to fines and other penalties. – Hindenburg Research

*https://hindenburgresearch.com/ormat/

Loop Labs (Plastic Recycling)

Loop Labs has enormous hype around technology. Hindenburg Research describes it in the following way.

Loop Industries has never generated revenue, yet calls itself a technology innovator with a “proven” solution that is “leading the sustainable plastic revolution”. Our research indicates that Loop is smoke and mirrors with no viable technology.

As part of our investigation, we interviewed former employees, competitors, industry experts, and company partners. We also reviewed extensive company documentation and litigation records.

Former employees revealed that Loop operated two labs: one reserved for the company’s two twenty-something lead scientist brothers and their father, where incredible results were achieved, and a separate lab where rank-and-file employees were unable to replicate the supposedly breakthrough results.

Our 30-year chemistry expert called Loop’s independent review “non-technical marketing material”, “very misleading” and concluded that “implying that [Loop’s process] is easy, inexpensive, and cost effective based on their released information is just wrong.”

The review was run on four total batches of Loop’s process, yet data for several of these batches is reported with glaring inconsistencies or, in the case of one base chemical, incompletely reported. – Hindenburg Research

*https://hindenburgresearch.com/loop/

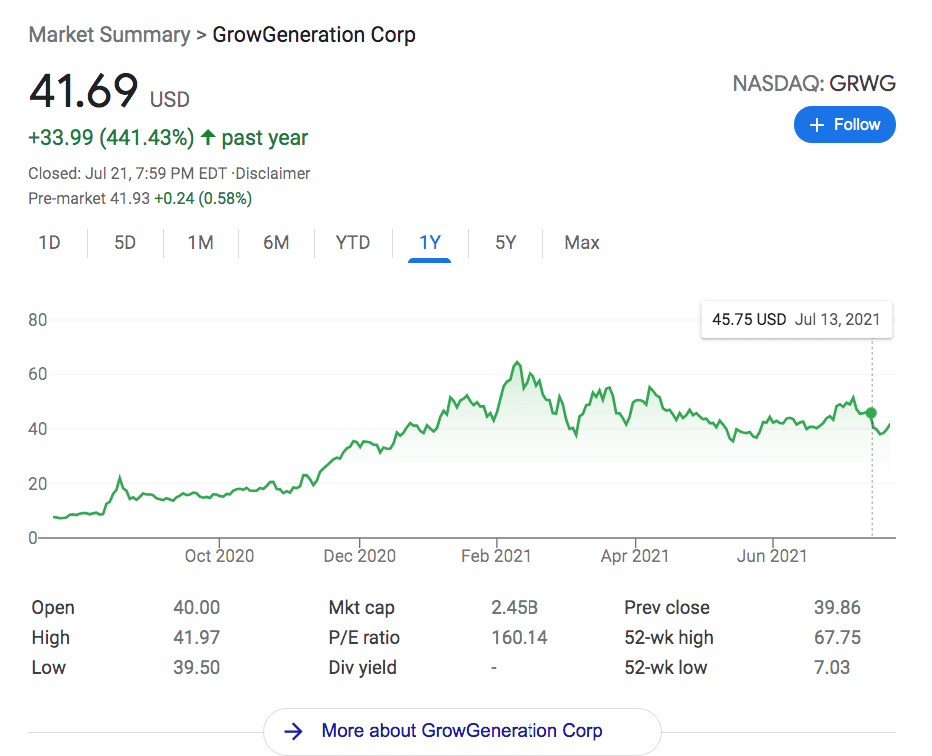

Grow Generation (Gardening)

The stock is priced absurdly rich even under a best-case scenario. This is clearly driven by retail momentum & euphoria.

President & Co-Founder Michael Salaman was alleged by the FTC to have engaged in scheme to sell consumer credit card information without authorization. He has an extensive career in penny stock failures alongside his father, Abraham Salaman, a twice-convicted fraudster with ties to the mob.

GrowGen is a roll-up of small mom and pop gardening shops. With the whole industry getting a financial temporary benefit from COVID-19, its stock has surged almost 108% in a week on the back of strong quarterly sales and retail investor enthusiasm.

GrowGeneration’s management team is one of the most questionable we have ever seen at a public company. Top executives have extensive ties to alleged pump & dump schemes, organized crime and various acts of fraud.

We live in extraordinary times, where a company like GrowGen can spike to almost a billion-dollar market cap largely on hype and pure retail momentum while major warning signs go largely unnoticed. – Hindenburg Research

Face Drive (Ride Sharing)

Facedrive recently went public with the core premise of being an “eco-friendly” ride hailing app that allows users to select electric or hybrid vehicle options. EV excitement has fueled the stock to a $1.4 billion market cap and an absurd 908x revenue multiple, making it the most expensive >$1 billion tech company in the world.

In an industry with virtually no technological barriers to entry, ridesharing companies are locked in an arms race to establish the largest rider & driver networks as the key competitive moat. After ~3 years of operation, Facedrive is nowhere close to making a dent. – Hindenburg Research

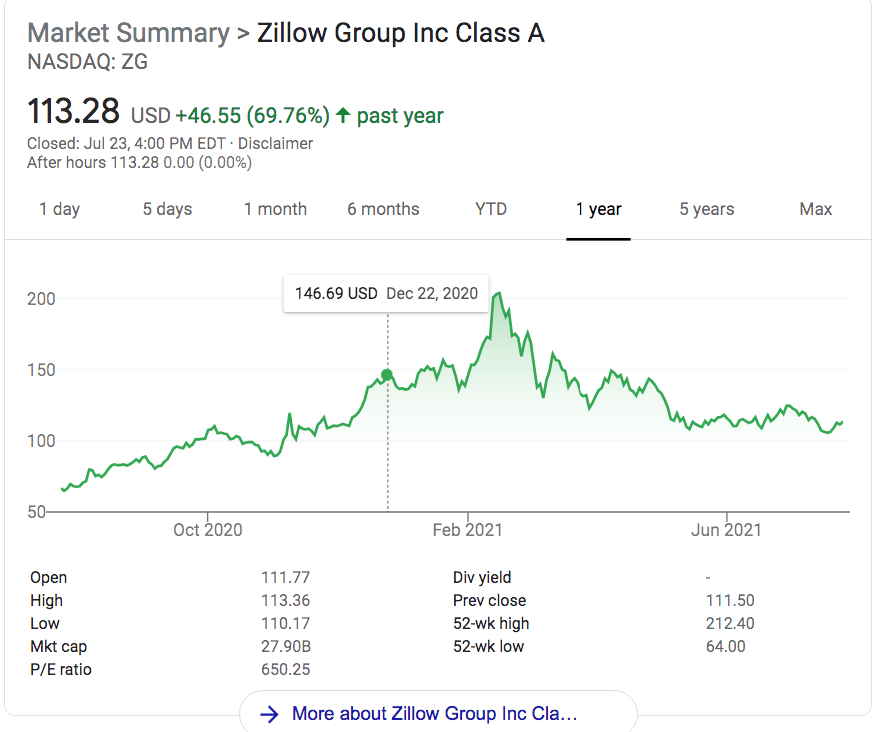

Zillow

Zillow is overpriced because it is based upon the real estate bubble.

Strategy: Short Some of These Stocks?

TBD.