Why is the Interest Rate on Savings Accounts Close to Zero?

Executive Summary

- For decades the US savings interest rate has been very close to zero percent, which lags the inflation rate.

- We cover likely reasons why the non-risk interest rate is close to zero.

Introduction

There is much discussion of the inflation rate, but little debate around the interest rate banks pay on savings accounts. What goes without notice is that every year, the US savings interest rate significantly lags the inflation rate.

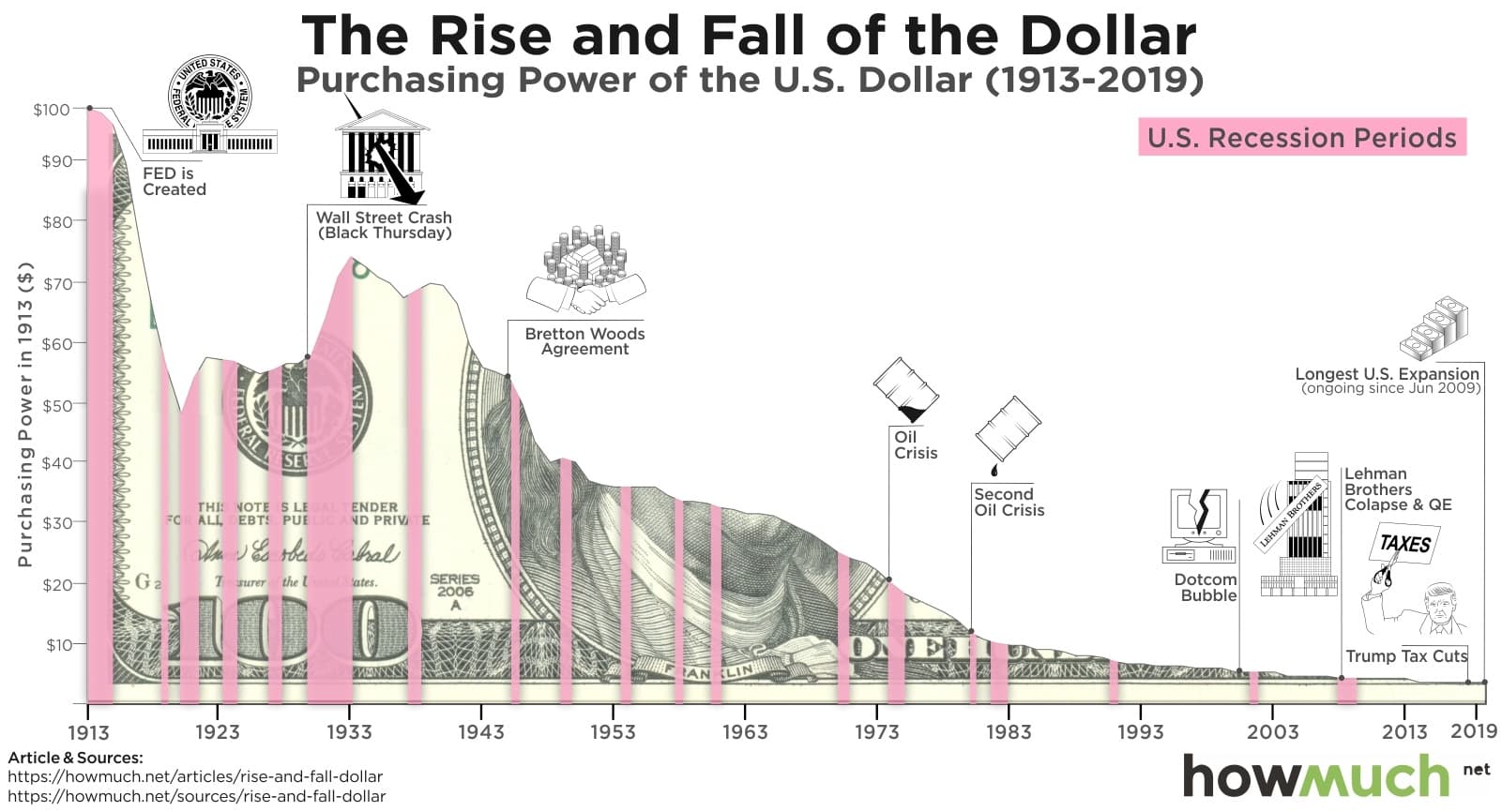

The Long Term Results of Inflation

A significant effect of those that do not want to put their money at risk is that it declines due to constant inflation. While a 2% inflation rate sounds small, over long periods of time, it has a very strong effect on the purchasing power of a currency.

Hold on to your money over a long period of time without putting it at risk, and the US government punishes you by eroding its value.

This image shows a shorter time frame and is a little easier to see.

This is covered by Wikipedia in the following quotation.

Over time, the compounded effect of small annual price increases will significantly reduce a currency’s purchasing power. (For example, successfully hitting a target of +2% each year for 40 years would cause the price of a $100 basket of goods to rise to $220.80.) This drawback would be minimized or reversed by choosing a zero inflation target or a negative target.

However, policymakers feel the drawbacks are outweighed by the fact that a positive inflation target reduces the chance of an economy falling into a period of deflation.

Losing on Retirement Money, Unless You Place the Money at Risk

The problem is that the interest rate in the US on savings of around .09%.

This is functionally 0%. This means that unless you put your money at risk, in the stock market, bond market, into other investments, you lose a little value every year and a lot of value over a long period of time. This is a curiosity and one which is barely discussed in the US in the media, at least. And that is, why don’t banks at least pay individuals the inflation rate so that they don’t lose their money?

What the banking system and the Federal Reserve are telling US citizens is to either risk their money or spend their money. Anything else, such as just saving money in a non-risk savings account, will mean losing the value of that money over time.

This is explained in the following quotation.

On the other side, a low inflation rate is often associated with economic weakness and nullifies some of the effect of monetary policy meant to stimulate the economy. Low inflation can lead to lower interest rates because when issuing loans or bonds, lenders will demand a premium to account for inflation. When interest rates are low, the Fed will often reduce the benchmark interest rate in order to encourage spending, consequently boosting the economy and preventing economic weakness.(emphasis added) As the benchmark interest rate gets very low and even approaches the zero lower bound, however, the Fed becomes increasingly powerless; they can no longer lower interest rates and expansive monetary policy becomes relatively useless and unfeasible. – Knowledge at Wharton

Notice that the interest rate is discussed, but the discrepancy between the savings interest rate and the borrowing interest rate (usually just referred to in articles as “the interest rate”) is not discussed. This is the established pattern, to ignore the discrepancy between the savings interest rate and the borrowing interest rate.

Need to Make Money On Interest Differential

Readers are consistently presented with the fictitious account that a bank must be able to make money on the loan but paying less on saving than it is being paid on the loan. This had nothing to do with how the US banking system works, because of what is known as fractional reserve banking, which is explained by the following quotation.

This is all the more peculiar because the financial sector already acts in many ways like a state franchise. The private money that it creates to invest, since banks lend far more than they actually have in deposits, only happens with the backing of the state itself. To make loans, banks borrow money from a central bank at a lower interest rate than they charge — and the central bank does this using a simple keystroke. – Jacob in Mag

It is rare to see this pointed out in articles, and this website is a small website.

Fractional reserve banking is explained in this video. But the fraction that is used in this video is far too high versus reality. In reality, the fraction that is required to be kept by the bank is less than 2%. This means that a bank only needs to pay interest on the 2% or fraction of the 100%. However, they charge interest on the rest. The secret to understanding fractional reserve is observing that the same money recirculates through the banking system. The power of fractional reserve banking is not on the initial loan; it encompasses all of the following loans made on the basis of the initial deposit.

At the time we watched this video, it was two years old, but had only 36,000 views. This is low for a YouTube video. Fractional reserve banking is of small interest to most people.

The banking industry likes it that way.

Savings Interest Rate Necessarily < Than Borrowing Interest Rate?

The best way of looking at this relationship is with a graph.

[wpgenially]https://view.genial.ly/5f215df4204af70d99164456/horizontal-infographic-diagrams-untitled-genially[/wpgenially]Very clearly, this means that the amount the bank pays to obtain money does not have to be lower than than the interest rate at which it loans out money. This is not explained to the public, and there are many people that work at banks that also are unaware of fractional reserve banking.

It is even more illustrative to almost think of the bank just making money. It needs only a tiny seed — which is deposits (or borrowing from other banks) to create money.

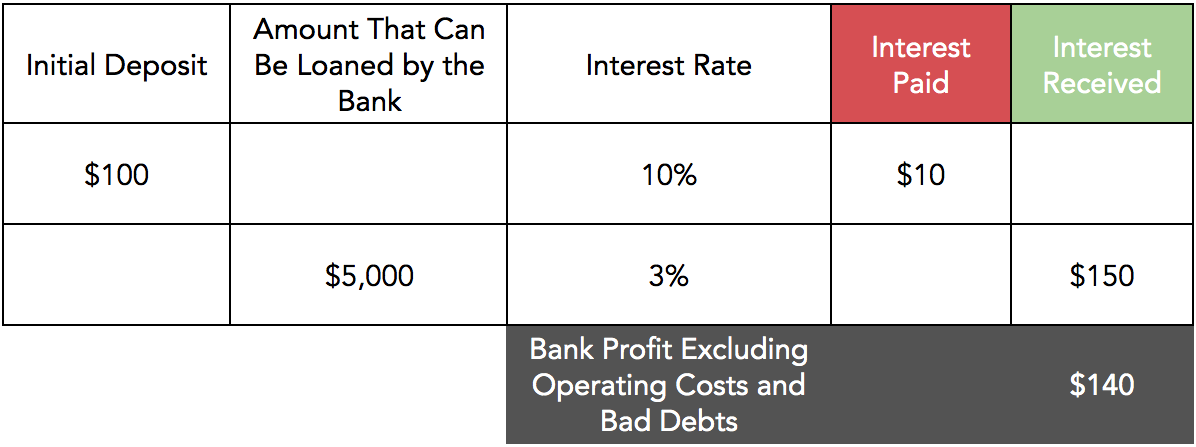

A Simulation of Banking Profitability Based Upon the Interest Rate Differential

This matrix shows how a bank could pay significantly more than their mortgage interest rate (so the lowest possible borrowing interest rate), and still make a great deal of profit. Naturally, banks have operating costs and bad debts. However, because of fractional reserve banking, the amount of interest paid is close to irrelevant to the bank, as the bank charges interest on far more money than it pays out interest on.

Printing Money or Creating an Entry for Money?

Often it is presented that only the US Government “prints” money. Printing money is now an anachronism as a physical currency is such a small percentage of all money that circulates. However, when one has a bank, they are granted that power as well. In this way, banks and credit institutions are extensions of the government. And most of the money that is “created” is created by private institutions loaning money, and therefore bringing money into existence.

Imagine if tomorrow the government said that if you had 1 or 2 dollars, you could loan out 100 dollars. And that all that was necessary was to create a debit on your computer and credit on another computer. If someone were to borrow $100 from you, then it would simply appear on that person’s credit card. If that person does not pay back the loan, you are required as a bank to write off the loan. That is really all that is going on with banking. It is a government-granted concession to privileged individuals and institutions.

How Banking Aligned Websites Explain the US Banking System

The following is a typical explanation of how banking works that are generally accepted.

One reason savings account rates are so low is that financial institutions profit when the rate on the money they lend out is higher than the rate they pay people who deposit money into savings. – Credit Karma

As we have seen, this explanation of banking is false. Credit Karma is an associated banking website, and as such, they naturally assume it is their responsibility to lie to consumers.

This false claim is repeated throughout many articles on this topic, as the following quote is essentially the same claim.

For the most part, a bank can offer whatever rate they want on a savings account. If one bank decided to suddenly start offering a 5% return on savings accounts, they certainly could do so. The only problem is that it would be a really bad business idea. Banks want some deposits in their savings accounts, but unless they can lend out money at a higher rate than they are offering on savings accounts, they’re not going to make money. They’re going to lose money. – The Simple Dollar

And they then continue to describe a different banking system than the one we have.

For example, let’s take a look at home mortgages. Right now, you can pretty easily get a home mortgage at 4 to 5% interest. In order to lend you that money, banks have to have that money (technically, they have to have a portion of that money because they can count the mortgage payments they’re going to receive… but that’s a whole different issue) in their vaults. In order to have that money, they have to have people depositing their money into that bank, and in order to get that, they have to offer some return on that deposit. At the same time, they have to offer less of a return on that deposit than they’re able to make from mortgages. So, the rate they offer has to be somewhere above 0%, but somewhere well below the 3-4% they get on mortgages.

Thus, we have interest rates on savings accounts hovering around 1%. – The Simple Dollar

This describes a full reserve banking system. But the US has a fractional reserve system. The US used to employ a full reserve banking system, but this was changed by the 1913 Federal Reserve Act, which also created the Federal Reserve (which is not part of the US Government, but a private entity)

This is a screen capture of the advertisements listed on The Simple Dollar website. If The Simple Dollar explained fractional reserve banking, and how depositors are being ripped off by banks, it is improbable this website would continue to receive advertising revenue. The Simple Dollar is not explaining reality to its readers, but what the banking system wants its customers to think is true.

Were Savings Interest Rates Always So Low Versus Inflation?

The answer is no, which is another reason the explanations provided by the faux financial education websites cannot be true.

This is explained in the following quotation.

When i was in junior high, my small town bank savings account at First National Bank paid 5.4% interest. I remember exploring opening a Swiss Bank account (i had great aspirations) and was disappointed it only got 4%. But both were above the rate of inflation. As George Bailey explained to me (It’s a Wonderful Life), my bank lent the money to other people in my small town, who built houses and paid back interest, part of which, i would get!

These rates would be unheard of in the 21st century. My current bank savings account pays .1% or less. Doesn’t my bank still lend out money to build houses, then collect interest and give part of it to me? – Reddit Comment

The Obsession, the Finance Industry, Has With Focusing Attention on the Mortgage Borrowing Interest Rate

Credit Karma makes the following statement.

When rates on loans are low, banks like to keep savings account rates even lower to continue making money on them. – Credit Karma

Again not true.

And borrowing interest rates are not all low. Many people are being charged far more than the mortgage lending rate, which is currently at roughly more than 3%. Many people are paying 20 or 30% on credit cards, with the current usury cap set to 36%. (70% of states have a 36% borrowing interest rate cap, which is why interest rates are often set to 35.999%). Delaware, where nearly all credit card companies are located as an exception on any interest rate cap if the loan is more than $10,000. And there are other problematic loans like payday loans, that somehow manage to charge 300% interest. However, to the banking industry, none of these other borrowing interest rates are worthy of discussion — no, they want everyone to focus on the mortgage borrowing rate.

This is another falsehood told by the banking and credit industry that tries to center the rate changed around the mortgage lending rate, which is the lowest rate of borrowing interest that exists.

Another reason some banks may not need to offer higher interest rates is that they’ve already won a large share of customers and aren’t competing aggressively with other banks for new business, according to research by Itmar Drechsler, a professor of finance at the University of Pennsylvania. – Credit Karma

That makes no sense.

If banks actually competed on the interest offered, some banks would raise their savings interest rate and attract deposits. The fact that they don’t mean that the savings rates are so depressed indicates that the banks are colluding with one another to keep the borrowing rate down. But secondly, because of how low the reserve requirements are, very little in the way of deposits is required in the first place.

People I know complain about how low the interest rates are on their savings account. If I had the opportunity to make a substantially higher interest rate on my savings, I would switch banks — as long as that bank was not horrible in other ways (i.e., I would not want my money with Well Fargo or Bank of America or Citibank, etc..)

This collusion by banks to depress savings interest rates is why the government should set savings accounts at least indexed to the level of inflation. This is a rigged system, and it has nothing to do with markets. And without a reasonable savings interest rate being Federally-mandated, banks get to pay less than nothing (remember the real savings interest rate is negative, as it is lower than the inflation rate in most years) to their deposit holders.

The gaslighting by Credit Karma is truly amazing. Here is their explanation of how to deal with these “totally rational and market-driven” interest rates on savings accounts.

Although interest rates on savings accounts are often low, you can find higher rates if you shop around. Online banks are a good place to start.

What I get from loaning my money to a bank, will not even keep up with the rate of inflation. My return is not $9.07, as shown in the high yield savings account. It is actually zero when adjusted for inflation. Should a savings account that does not even return the rate of inflation be called “high yield?”

What else can someone say but, “Thank You, Credit Karma!”

Is this an independently written article, or simply what Citibank and Bank of America would like us to accept as true?

Keeping the Banking Customer in the Dark

Banks never explain fractional reserve banking to their customers. Therefore customers consider it reasonable that the interest rate on their savings is less than the borrowing interest rate. Banks use the secrecy around fractional reserve banking to justify the paltry savings interest rates they provide. In reality, the US Government could mandate that the savings interest rate always be higher than the inflation rate, and banks would be just fine. But they do not do this. They don’t do this because the US Government represents the banks far more than they represent the public.

Conclusion

The fact that in the US at least, interest rates on savings accounts (that is non-risk interest rates) are so close to zero, and lead to the loss of value every year for individuals who are not willing to risk their principle undermines the argument by the Federal Reserve or the banking system that there is a genuine concern for the citizens. The fact that the non-risk interest rate on savings around is roughly 2% lower than the inflation rate means that ordinary citizens are providing a subsidy to banks. This adds to the money-making ability of banks that have the power of fractional reserve banking. It would seem that a basic tenant would be that the interest rate on savings accounts would not only match inflation but would also not be taxed (why are capital gains being paid to the government if there are not REAL capital gains being made)? That is, it would seem capital gains should only be charged on returns after inflation is removed.

References

*https://www.creditkarma.com/savings/i/why-are-interest-rates-low-on-savings-accounts#

*https://www.reddit.com/r/investing/comments/dqrcwu/why_are_bank_savings_account_interest_rates_so/

https://www.forbes.com/sites/billconerly/2017/10/17/why-are-banks-paying-so-little-interest-on-deposits/#721ef95556c3

https://www.nclc.org/images/pdf/pr-reports/why36pct.pdf

*https://www.nytimes.com/2020/05/15/business/strategies-investing-interest-rates.html

https://www.jacobinmag.com/2020/06/wall-street-coronavirus-pandemic-recession

https://www.bls.gov/cpi/questions-and-answers.htm

This explains how dollar inflation is a hidden tax. Having the savings rate be lower than the interest rate is critical to maintaining this hidden tax.

This video describes the creation of the Federal Reserve and the move to fractional reserve banking.

For details on how the Federal Reserve in unconstitutional see the article How the US Federal Reserve is Unconstitutional and Its Current Corruption Was Predicted.