How to Understand Why ERP Systems Have a High TCO and Low ROI

Executive Summary

- ERP is sold on the basis of its unsubstantiated financial benefits.

- Find out why ERP systems have a high TCO and normally a negative ROI.

Introduction

The Wikipedia definition of the total cost of ownership (TCO) is as follows:

Total cost of ownership (TCO) is a financial estimate whose purpose is to help consumers and enterprise managers determine direct and indirect costs of a product or system. It is a management accounting concept that can be used in full cost accounting or even ecological economics where it includes social costs.

See our references for this article and related articles at this link.

Background on TCO

We find TCO research incredibly illuminating. TCO is one of the most misunderstood, abused, and underutilized tools for enterprise software decision-making. Our work on TCO has provided us with insight across multiple software categories. It is a mistake to limit the use of TCO to such a narrow range of decisions. Because we perform TCO for so many software categories, we know the following:

- How the TCO varies based upon the size of the implementation.

- The TCO varies based on the delivery method (SaaS or on-premises).

- How TCO varies based upon the complexity of the implementation.

- The average percentage that one can expect the implementation to cost for any one specific cost item or cost categories such as implementation, license, hardware, or maintenance and support.

- ERP combined with 100 percent ERP vendor applications.

- ERP combined with 100 percent best-of-breed solutions.

- Open source ERP, 100 percent best-of-breed solutions.

- No ERP, 100 percent best-of-breed solutions.

- The risks of various software categories.

False Assumptions of ERP

The analyses include assumptions often not considered, such as realistic average implementation times. These implementation times, habitually underestimated by vendors and consulting companies, have been taken from actual projects. I can say unequivocally that from this database of knowledge, we have disproved many deeply entrenched concepts that drive IT decisions to poor outcomes. In our view, combining unbiased and highly detailed TCO calculations and evaluating comparative software functionality based on strong domain expertise are two of the most critical inputs to producing quality IT decisions.

Unfortunately, this knowledge is not resident within companies, and ERP software vendors (as well as consulting companies and IT analysts) have not informed companies as to the true TCO of ERP systems; it takes work to do this analysis, and probably more importantly, the ERP vendors do not want to buy companies to know.

Various ERP TCO Studies Versus Our Estimates

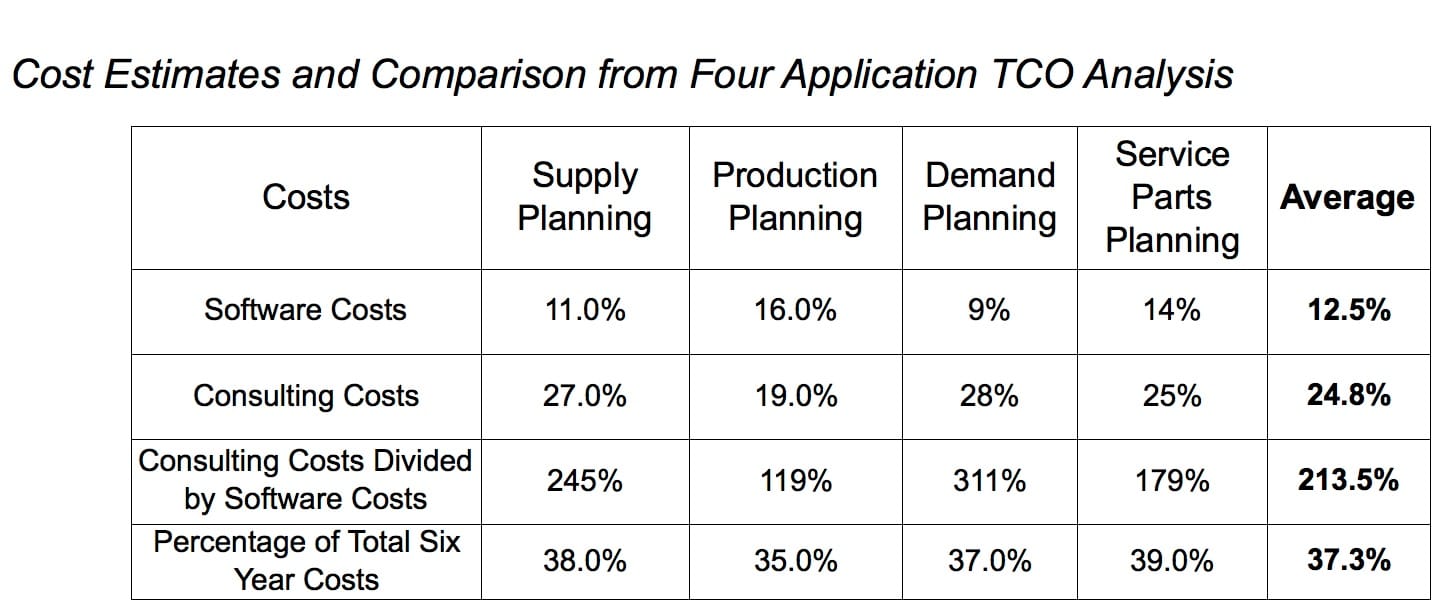

The study What Managers Should Know About ERP/ERP II estimates the costs of ERP software licenses to be between 10 and 20 percent of the overall TCO, which is higher than we estimate. While the software license cost of most application categories averages 20 percent of the TCO, we estimate that 8 percent of the TCO of Tier 1 ERP software is due to software license costs. ERP implementations take so long and have so much customization and maintenance expense. So it’s not that the software license cost is lower; the TCO is made so much more significant by the customization and implementation expenses that the software license cost becomes a smaller percentage of the cost in comparison. The book Control Your ERP Destiny: Reduce Project Costs, Mitigate Risks, and Design Better Business Solutions considers a reasonable estimate of the costs of ERP software to be 20 percent of the total project budget. According to this book, software vendors provide their potential customers with estimates (as do consulting companies) that consulting costs will be roughly twice the cost of the software. One independent source, called 180systems, actually estimates that consulting costs average 65 percent of the license costs (71 percent for larger customers and 59 percent for mid-sized customers). Below is a meta-analysis and comparison of my individual TCO analyses.

While the software vendor estimate of consulting costs holds true for my sample (although you can see that there is considerable variability), this does not correlate with our estimations because other TCO estimations that we have reviewed consistently underestimate the TCO of applications. Because license costs are explicit costs, they are the easiest to estimate and, thus, the easiest to overestimate in relation to other costs.

Estimations from other sources are all over the map. Some entities recommend a rule of thumb of 1:1 between license and consulting costs. The software vendor e2benterprise recommends a ratio of between 1:3 to 1:4. We worked backward from these numbers and found that the estimations on the software license costs are solid, but the ratio of 1:4 only estimates consulting; it does not bring the total ERP cost even close to the estimations of the total costs of ERP. Additional costs, such as vendor support, hardware, and ongoing maintenance, are well known. It isn’t easy to see why so much emphasis is placed on the software and implementation costs while maintenance costs are left out. Hardware costs are barely worth mentioning as they represent a small percentage of the overall TCO, but estimated maintenance costs must be included in decision-making.

The Brightwork Research & Analysis Estimates

Our website estimates software, hardware, implementation, and maintenance costs—both external and internal costs. Maintenance costs are incurred to keep the applications running, but they also include maintenance of customizations. As 96 percent of ERP implementations require moderate or heavy customization, work is required to keep customizations up-to-date with new releases and augment the customizations, making ERP software maintenance a high cost. An important aspect of evaluating ERP TCO studies is that the consulting expenditures on most ERP projects are significantly over budget, which ERP software vendors would not have included in their TCO estimates.

Generally speaking, a 100 percent success rate is assumed for implementations (strange, as the actual success rate is far lower than this) when vendors estimate TCO for ERP and enterprise software. However, if the project goes over budget or fails, the estimates provided by the software vendor do not apply, nor do our estimates. We have observed this as a problem regarding how projections are performed, and I explain this in the book Enterprise Software Risk: Controlling the Main Risk Factors on IT Projects. We are currently developing risk estimators for all analyzed applications; these risk estimates are auto-adjusted based on the application, the consulting partner used, and the stated capabilities of the company. The company can perform its interactive analysis right on our website.

Is the TCO of Failed Implementations Included?

What is the TCO for software that is never implemented? I have interviewed for several projects (and worked on a few) re-implementations where the software failed to go live.

That failure may have taken a year and a half; the company focused on other things and then decided to re-implement the software two and a half years after it began the first implementation. If the software is taken live the second time, most likely, the project will have a negative ROI. The standard ERP TCO calculators we provide would not apply. Therefore, anyone interested in ERP estimation should ask: If 60 percent of ERP implementations fail, and if the vast majority of ERP implementations miss their deadlines by significant durations, why are TCO estimations still based upon assumptions that do not include these critical factors?

There is little disagreement on the fact that companies repeatedly underestimate the costs of ERP systems.

“In ERP systems, having clear criteria for success is particularly important since the cost and risk of these valuable technological investments must be reviewed in light of possible payoffs. Mabert, et al. (2001) put the total ERP implementation cost at tens of millions of dollars for a medium-sized company and $300 to $500 million for large international corporations.” — Measures of Success in Project Implementing Enterprise Resource Planning

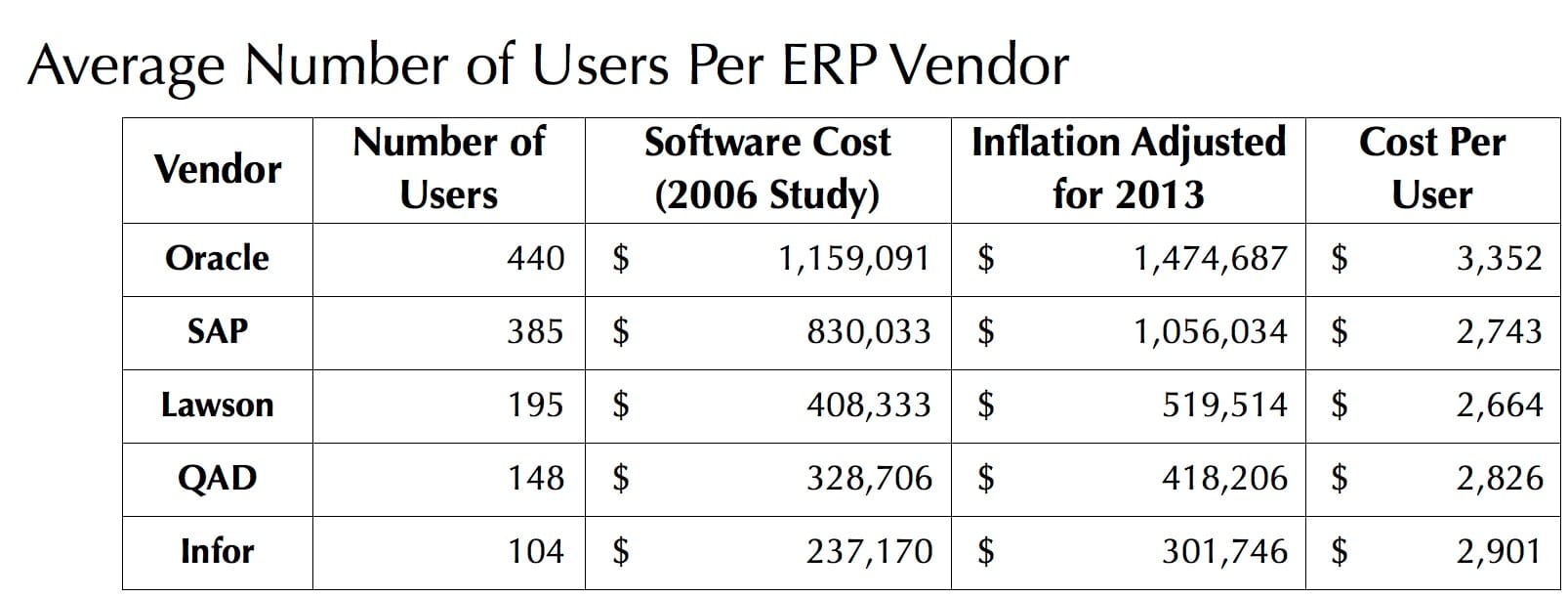

According to Aberdeen, the average number of users per ERP software vendor is as follows (we used Aberdeen’s numbers for this purpose, although Aberdeen’s TCO studies were not used in this book):

Significant price differences exist if just the aggregate license revenues are compared among ERP vendors. However, this difference in license revenue is primarily driven by the differences in the average number of users. On average, the Tier 1 ERP vendors, such as Oracle and SAP, have a much larger customer base, as measured here by the number of users. This relationship is so strong that a regression between the number of users and the software cost results in a 96.75 R Squared, as the following graphic shows. Microsoft’s average number of users is more comparable to Lawson, QAD, and Infor than Oracle and SAP.

Even though it is well known that ERP does not lower costs, the actual cost of ERP goes well beyond the direct cost of the software but extends to the indirect costs such as the costs of maintenance, the costs of adjusting the functionality in other systems to make it compliant with how ERP works, to increased needs for customization, to losses in inefficiency as mediocre ERP functionality is used in place of better functionality that could be obtained by buying specialized software. Most companies did not perform TCO analyses before purchasing ERP systems. It is now long forgotten that ERP systems were sold based on the concept that they would lower costs (the idea that an ERP system could have a low TCO is laughable even today). Since then, ERP systems have proven to be very expensive, not only to implement but also to maintain, as the following quotation explains.

“ERP systems were expensive, too, costing companies more than they had ever paid for software when costs had been based on per workstation usage. But that price tag was dwarfed by the installation charges, because companies had to hire brigades of outside consultants, often for a number of years, to actually get the software up and running. While the average installation cost $15 million, large organizations ended up spending hundreds of millions of dollars.” — The Trouble with Enterprise Software

How Mistakes Concerning ERP

The long-lived mistakes concerning ERP have affected every part of IT today. ERP systems have proved to be much more expensive than even the highest “generalized” cost estimates (even though 80 percent of the time, companies did no accurate estimation). ERP systems now consume a substantial portion of the overall IT budget, particularly for companies that purchase from the most expensive Tier 1 ERP software vendors. The high investment in ERP negates investment in other possible applications, even though most of these other applications would have a higher ROI than ERP. All ERP ever offered was basic functionality, and any company that has basic functionality consuming the majority of its IT budget has a severe problem with resource allocation. By that measure, an enormous number of companies have this problem. The direct cost of ERP systems has continued to increase. When companies give so many modules to one vendor, they also give up a lot of negotiating leverage. The ERP vendors use this leverage to:

- Sell uncompetitive software in other areas of the same account.

- Increase the cost of the yearly support contract. The TCO of on-premises ERP systems is generally considered high compared to other application categories. It is quite remarkable that writers who cover ERP implementations do not frequently bring up these issues. Various articles will discuss how expensive ERP systems seem, but the enormous elephant in the room—the leverage of ERP vendors—is unaddressed.

The Influence of the Length of Implementation Times on the ROI of ERP Systems

ERP systems have very long implementation times and a high run rate in costs.

The ERP Implementation Duration

The implementation time for ERP systems is the longest of any enterprise software category. The term “implementation time” is laden with assumptions. At our site, we perform risk and duration estimation for all major enterprise software categories. ERP has by far the most extended implementation of any software category—and by a wide margin.

Furthermore, ERP software comes with high risks for implementation. According to IDC, 15 percent of survey respondents implemented their ERP software again. What was the implementation time on those projects? It is not easy to find detailed TCO studies on ERP systems, which is one of the reasons we began estimating it on a separate website. ERP ROI The ROI of ERP is an exciting topic; as expected, a company implementing an application with a very high TCO is disadvantaged when obtaining a high ROI.

“A Meta Group study of sixty-three companies a few years ago found that it took eight months after the new system was in (thirty-one months in total) to see any benefits. The median annual savings from the new ERP system were $1.6 million—pretty modest, considering that ERP projects at big companies can cost $50 million or more. ERP systems may be integrated, but on-premises ERP has proven to be poor at integrating to other applications and to business partners.” — The ABCs of ERP

“Markus, et al. (2000) argued that the companies that adopted ERP systems need to be concerned with success, not just at the point of adoption, but also further down the road. After ERP implementation is complete, the expected return may not come as soon as desired. In fact, most ERP systems show negative return on investment (ROI) for the first fi ve years that they are in service.” — Measures of Success in Project Implementing Enterprise Resource Planning

This is quite a statement.

And the implications of this statement cannot be understood without performing a little math.

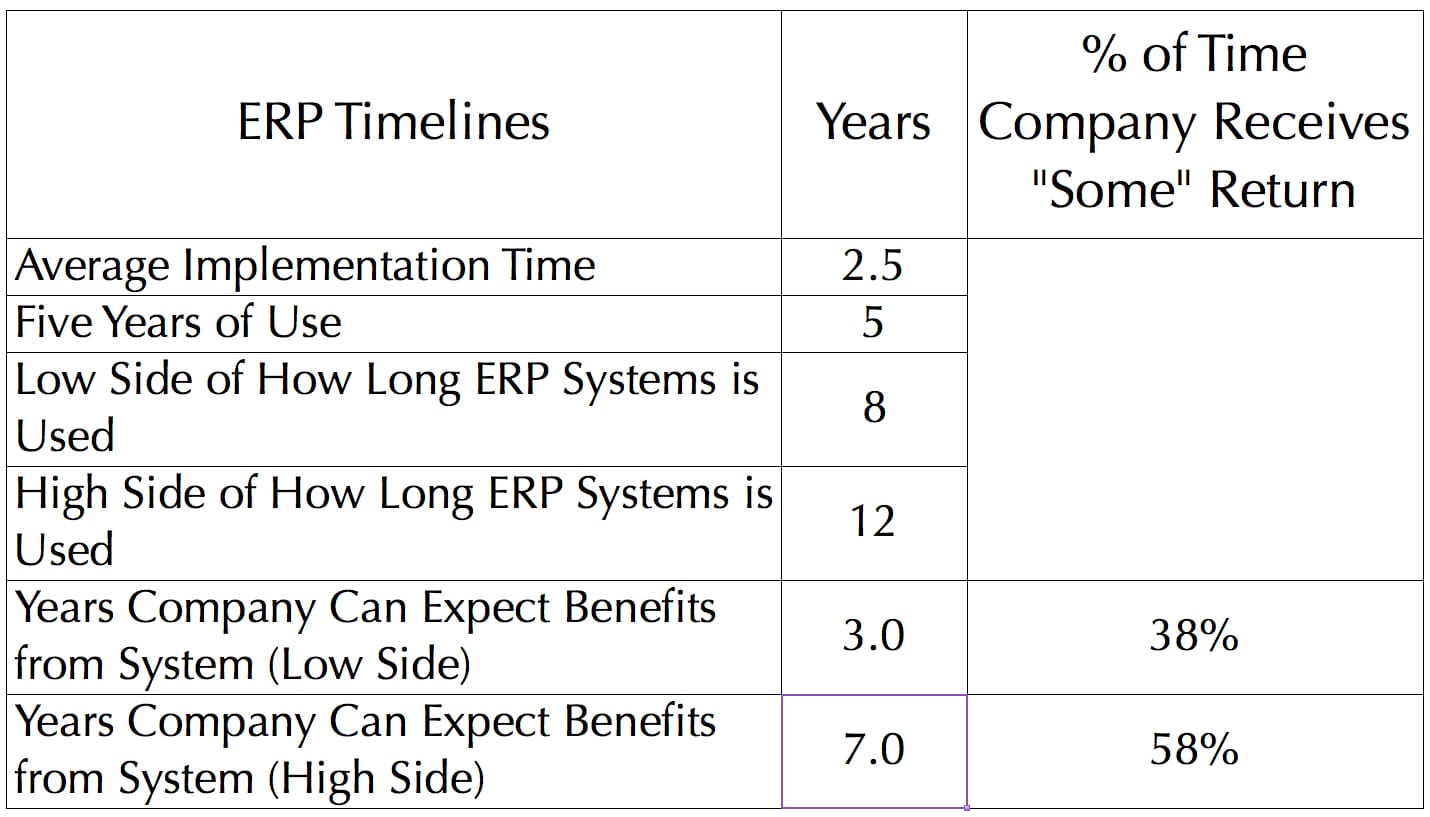

The math presented above is problematic when one compares the known estimated durations with ERP. Generally, ERP systems are thought to have a useful life of between eight and twelve years. If it is true that no return can be expected for the first five years of use, it is seven-and-a-half years into the ERP project when the company has begun paying for the ERP system (including two-and-a-half years of implementation time).

If the ERP system is decommissioned after eight years, the company has three years to receive a return (which would mean a negative ROI). If the ERP system is decommissioned at the high side (after twelve years), there are seven years, or 58 percent of the total time, that the ERP system is in the company to receive a return. While the information up to this point is problematic, the news gets worse with the following statement.

“After the first five years of use, a company can expect steady returns, but not in the traditional form of revenue. As Markus and Tanis (2000) indicated, different measures are needed at different stages in the system lifecycle and a minimum set of ERP success metrics should include projects metrics, early operational metrics and long-term business results.” — Measures of Success in Project Implementing Enterprise Resource Planning

According to this quote, there are close to no financial returns, which is what studies generally say. Researchers think no return can be expected until seven-and-a-half years after the ERP project kick-off. While no financial return can be demonstrated, it is implied that ERP pays off in other ways that are imperceptible to the company’s financial health. The company may not be able to expect a return until other applications are connected to the ERP system.

Selling the Dream…..of ROI on Related Items

“‘There’s a general understanding today that ERP is the investment you have to make just to get into the game,’ says Josh Greenbaum, a principal analyst with Enterprise Applications Consulting. ‘First you have to get ERP installed, and then you can take a look around and see where major ROI can be achieved. It’s the so-called secondwave applications, such as business intelligence, supply-chain management, and online procurement, that can leverage the ERP backbone and offer the highest return,’ says Greenbaum.” — Making ERP Add Up

That is one incredible statement. Talk about “future selling.” There is no evidence that ERP improves the benefits/return on investment from other applications; this is utter conjecture on the part of this Jeff Greenbaum — who I later discovered is an industry shill and paid by vendors to pretend to be independent and is often quoted in the IT media — the major vendors also pay that.

Then comes the other issue with estimating operational benefits, as the following quotation explains.

According to Parr and Shanks (2000) ‘ERP project success simply means bringing the project in on time and on budget.’ So, most ERP projects start with a basic management drive to target faster implementation and a more cost-effective project… Summarizing, the project may seem successful if the time/budget constraints have been met, but the system may still be an overall failure or vice versa. So these conventional measures of project success are only partial and possibly misleading measures when taken in isolation (Shenhar and Levy, 1997). — Measures of Success in Project Implementing Enterprise Resource Planning

With such high costs, ERP consumes much of the overall IT budget. According to Forrester and Gartner, the maintenance of ERP systems consumes 50 to 90 percent of the IT budget. As with any other software, ERP software consumes resources across all IT operating budget categories. ERP has proven to be an expensive proposition for companies and has not reduced costs as promised by its proponents. The problem is that both ERP systems’ direct AND indirect costs have been high.

The Low (and Misleading) ROI of ERP Software

It is difficult for ERP to have a good ROI if it also has a high TCO. The TCO is the denominator in the ROI equation, with the business benefits being the numerator. Another problem with ERP ROI is that ERP systems take a long time to implement. Other estimations are shorter, but I have not found any research that provides a solid method for this analysis. I quote this book’s estimate not because it explains or divulges its data points but because I find the book credible in other aspects. However, even this book’s estimates are lower than those of the study by Meta Group, which proposed that it would take eight months until the ERP system begins showing any benefit. This figure is contradicted by the study The Impact of Enterprise Systems on Corporate Performance, which states that after ERP implementation, the company lost productivity every year when the ERP system went live. (This study is discussed on the next page.) If we take the lowest estimate and average the high and the low values, we get the following:

((12 + 36 months)/2 + (4 + 6 months)/2) = 29 months 29 months / 12 = 2.4 years

According to the above calculation, a company must pay for an ERP implementation for two years and then wait another five months before the software is functional to the degree that it can be relied upon. That is taking the average of the most optimistic of the three estimates; other scenarios are not even this rosy. For instance, one scenario is that the company never sees any productivity benefit even though it implements the ERP system. Another scenario is a 40 percent likelihood of significant disruption to business operations during the go-live. What is the cost of this “major disruption”? Well, that is not estimated. What about more minor disruptions? It would seem quite likely that more minor disruptions occur with even greater frequency; however, I have never seen a TCO analysis for ERP that includes the costs of these disruptions. An exciting timeline was provided in the paper Which Came First: IT or Productivity? Where a complete timeline of an ERP implementation, as well as the software that followed it, was laid out.

This shows a relatively fast ERP implementation timeline of nineteen months from the ERP system kickoff until the full go-live. However, this company would not have seen the full benefit of ERP until the ERP system was fully integrated, which is not mentioned in this study.

Most estimates are unreliable because they are put out there by consulting companies or ERP vendors themselves. Generally, what is not debated is that ERP software takes the longest of any software category to implement. Furthermore, most estimates of ERP implementation timelines leave out the time to integrate other applications into the ERP system. Gartner estimates that it can take up to five years to integrate the other applications within the company into the ERP system. Because the full benefits of an ERP system are not realized until ERP is integrated into all the company’s various applications, the value realized is incremental up until then.

The Problematic Logic of ERP-Driven Improved Financial Performance

Our research into the studies of ERP ROI shows the following:

- ERP implementations show no positive business benefit and often impose high costs (e.g., missed orders due to lack of inventory and inability to ship orders that are received due to execution problems).

- The potential for ERP implementations to show a positive business benefit for up to a year after implementation is low, as the company is still adjusting to the radical changes that an ERP system imposes on a company. Once these problem projects are thrown into the mix, the average return for an ERP planning project is harmful.

While there is no research into the ROI of ERP software, one would assume that ERP would generally have a poor ROI for the reasons listed above. Others, such as the Sloan Management Review, have noted this lack of ROI research:

“Given the high costs of the systems—around $15 million on average for a big company—it’s surprising…that despite such study, researchers have yet to demonstrate that ‘the benefits of ERP implementations outweigh the costs and risks.’ It seems that ERPs, which had looked like the true path to revolutionary business process reengineering, introduced so many complex, difficult technical and business issues that just making it to the finish line with one’s shirt on was considered a win.”

This begs why, as stated in the above quote, “ERPs…had looked like the true path to revolutionary business process reengineering.” The answer to this question is simple: several entities with a solid financial bias declared it so.

Negative ROI: The Missing Link of the ERP ROI Research

Every research study into the ROI of ERP systems that I reviewed (except for the research that attempts to find a correlation between ERP implementations and the financial performance of companies) contains several flaws. Some of these flaws have been stated in this book and relate to an underestimation of the TCO, as described in the previous section. If the TCO is not conclusive, then the ROI is inaccurate; the TCO is the base or the “I” in the ROI. Let’s review the issues with estimations of the TCO (usually overlooked ones) before examining the error from the return side.

- The TCO for ERP projects is not adjusted for risk.

- The total length of ERP projects is not included in the TCO calculation. The longer the project, the longer it takes to repay the investment. Furthermore, ERP projects are so problematic from the integration perspective that it can take up to five years for them to be fully integrated with other systems and, therefore, fully operational.

- There is a 40 percent likelihood of a major operational disruption after an ERP project goes live. The costs of these significant disruptions nor the costs of smaller disruptions are included in the ERP TCO calculations.

- ERP TCO estimations consistently underestimate the actual TCOs of projects. These estimations completely neglect or underestimate the costs of internal resources to adjust to and learn the ERP system. This issue is not specific to ERP software but is generally a feature of enterprise software. However, the large-scale nature of ERP software makes this issue worse.

The error on the return side of ROI is that ERP ROI studies look at the ERP system in isolation from the other software the company implements. However, as will be explained in more detail in “Case Study #4 of ERP Misuse: Intercompany Transfer”, the transactional inflexibility of ERP systems—the fact that they have their modules so tightly integrated—restricts a company’s ability to fully leverage the functionalities in applications that are connected to ERP systems. As a result, a company with an ERP system will receive less value from other applications they implement (unless the application is extremely simple) than a company that does not have an ERP system. Companies with ERP systems do not leverage the other applications they purchase and implement, so they must use more of the mediocre functionality within the ERP system. I found this statement by Aberdeen very interesting:

“As ERP has become more pervasive, there is always a risk in perceiving it as necessary infrastructure. If viewed as a requirement for doing business, companies also run the risk of neglecting to measure the business benefi ts resulting from its implementation.”

I would say this statement is a bit late. The decision to purchase ERP was not based on measuring its business benefits but primarily on the idea that ERP systems were “necessary infrastructure.”

Support Costs of ERP

The maintenance costs of Tier 1 ERP (and possibly other tiers) are likely headed upward. ERP software is stabilizing and falling further behind the other connected applications, which can replace much of ERP’s functionality. Instead, SAP moves almost all of its newer functionality to its non-ERP modules, as it can charge new license fees. Analysts are not picking up on this, but investment in ERP has wilted, and ERP systems cannot meet requirements without further customization. Your ERP vendor already has your ERP business; they want to nudge up the ERP support costs, and they have some other software they want to sell you. The High

Opportunity Cost of ERP

The opportunity costs of ERP are underemphasized (or ignored altogether). The term “opportunity cost” is used infrequently, so let’s define it before we explain how it should be used in making decisions:

“In microeconomic theory, the opportunity cost of a choice is the value of the best alternative forgone, in a situation in which a choice needs to be made between several mutually exclusive alternatives given limited resources. Assuming the best choice is made, it is the ‘cost’ incurred by not enjoying the benefit that would be had by taking the second best choice available.” — Wikipedia

Generally, costs are often described as the amount we pay for things. Economists look at costs quite a bit differently. Opportunity cost is one cost category and sunk cost.

Promoters of ERP tend to present any benefits of ERP without acknowledging that the time and effort spent on ERP could have gone into other initiatives. However, the gain from those systems should be compared against the gain from ERP systems.

Let’s take a simple example. Imagine that I have no car. I have a hard time getting around town because I lack transportation. To improve my condition, I buy a Hummer. After a week, I report that I can get around town much more efficiently, and compared to walking, I am now much more mobile. Have I established that the Hummer was the best possible alternative? I have not proved this. I could have purchased any car—almost any of them with lower operating costs than a Hummer. Therefore, the question is not whether the purchase of the Hummer improved my condition compared to the other alternatives (these alternatives could have included any other car of equivalent or lower cost, public transit, bicycle, etc.). Does my analogy that a Hummer is the best automobile one can buy sound silly? Well, it should, but it is no sillier, no less evidence-based than the evidence presented for why ERP has helped companies. The comparison can never be between “something” and “nothing” but between two “somethings.” People who compare something to nothing are stacking the deck in favor of the “something” and are not promoting research or a logical and severe framework.

The Logic of ERP-Driven Improved Financial Performance

Enterprise software implementations should have a positive ROI. This is why they are purchased. In this section, I will provide a synopsis of the research findings.

“The results are based on a sample of one hundred eighty-six announcements of ERP implementations; one hundred forty SCM implementations; and eighty CRM implementations. Our analysis of the fi nancial benefits of these implementations yields mixed results. In the case of ERP systems, we observed some evidence of improvements in profitability but not in stock returns. “The results for improvements in profi tability are stronger in the case of early adopters of ERP systems. On average, adopters of SCM system experience positive stock returns as well as improvements in profi tability.” — The Impact of Enterprise Systems on Corporate Performance

This makes sense because ERP functionality was more advanced in the past. Now, the technology of almost any on-premises ERP system will be quite dated. Secondly, at one time, an announcement that a company would implement an ERP system would have affected stock prices because the system was considered a leading edge. However, ERP systems are so common now that a bump in stock price can no longer be expected. Interestingly, the improvement in financial performance for ERP lagged behind SCM implementations. Compared to other implementations, ERP consistently lags behind other enterprise software categories.

The Stock Price of Firms that Invest in ERP

“The evidence suggests that over the five-year period, the stock price performance of firms that invest in ERP systems is no different from that of their benchmark portfolios.” — The Impact of Enterprise Systems on Corporate Performance

This means that investing in an ERP system did not impact the companies’ stock prices in the study.

“The positive changes in ROA (Return on Assets) during the implementation period are statistically signifi cant at the 5 percent level. Although the changes in ROA during the post implementation period are positive, none of the changes are statistically signifi cant. Overall the evidence suggests that although fi rms that invest in ERP systems do not experience a statistically significant increase in stock returns, there is some evidence to suggest that profi tability improves over the combined implementation and post-implementation periods.” — The Impact of Enterprise Systems on Corporate Performance

ERP Versus SCM ROI?

While the financial benefits of ERP investments are either nonexistent or barely perceptible, the results of SCM software investments were positive; while investments in CRM software were the same as ERP, they did not show gains. Furthermore, clients who were early adopters of ERP achieved better returns, which means that the returns of companies that have recently implemented ERP are even worse.

“The results for the accounting metrics provide strong support that fi rms that invest in SCM systems show improvements in ROA and ROS (Return on Sales). Improvements are observed in both the implementation and post-implementation periods, with mean and median changes in ROA and ROS generally positive and most are statistically signifi cant at the 2.5 percent level or better.” — The Impact of Enterprise Systems on Corporate Performance

ERP Versus CRM ROI?

Conversely, CRM scores very similarly to ERP implementations: no relationship to financial performance improvement can be found.

“Over the full four-year period, the mean (median) abnormal return is –15.22 percent (–12.41 percent), and nearly 53 percent of the sample firms do better than the median return of the firms that belong to their assigned portfolio. However, none of these performance changes are statistically significant. Basically, investments in CRM systems have had little effect on the stock returns of investing firms. These results are consistent with that of Nucleus Research (2002), who report that 61 percent of the twenty-three Siebel customers that they surveyed did not believe they had achieved a positive ROI.” — The Impact of Enterprise Systems on Corporate Performance

Overall ROI of ERP

“Despite the generally positive acceptance of ERP systems in practice and the academic literature, other studies have not found overwhelming evidence of strong positive performance effects from investments in ERP systems. Our results are generally consistent with these findings.” — The Impact of Enterprise Systems on Corporate Performance

“For example, although Peerstone Research (Zaino [2004]) found that 63 percent of two hundred fifteen fi rms gained ‘real benefi ts’ from adopting ERP, they also report that only 40 percent could claim a hard return on investment (ROI). Other ROI results are reported by Cooke and Peterson (1998) in a survey of sixty-three companies that found an average ROI for ERP adoption of negative $1.5 million.” — The Impact of Enterprise Systems on Corporate Performance

“Overall we find that, controlling for industry, ERP adopters show greater performance in terms of sales per employee, profit margins, return on assets, inventory turnover (lower inventory/sales), asset utilization (sales/assets), and accounts receivable turnover.” — ERP Investment: Business Impact and Productivity Measures

This last quote sounds convincing, although no numbers are listed, and there is no comparison of the financial benefit versus the implementation of another type of system. Furthermore, it is no longer possible to be an earlier adopter of ERP software; at this point, one can only be a late adopter, meaning the benefits of adopting ERP are lower. The data for this report was taken from companies before or during the implementation (before the system being live) and before when the system is operational and providing benefits to the company. This same report stated that the benefits of the ERP implementations began to reverse after the system was live. Here are the productivity gains from the same study.

“There is a productivity gain during the implementation period, followed by a partial loss thereafter. When value added is used as the dependent variable, the gains are 3.6 percent during implementation with a loss of 4.7 percent for a net gain of –1.1 percent (t=.8, not significant).” — ERP Investment: Business Impact and Productivity Measures

How Much Money Has Been Wasted on Oracle and SAP ERP?

The uncovered story of how ERP software became the most popular category ever developed within enterprise software. This was done without any evidence that it could either pay back the enormous investment it required or improve the return or efficiency of applications that were connected to it. Or even reduce the integration costs incurred by IT departments related to a central problem in IT decision-making, which is explained in the quotation from the book below:

- Accepting Simplistic Explanations: Companies tend to be easily influenced by oversimplified rationales or logic for following particular courses of action. This will repeatedly be shown in this chapter. If the executive decision-makers had known technology better and if they had studied the history of both enterprise software sales methods, there is no way that the simple logic that was so effective in selling ERP would have worked. Another way of looking at this is that it was simply all too easy.

The Team Effort Required for the Analytical Failure

It was a team effort to make such poor decisions, and the research shows repeated unsubstantiated comments made by IT analysts and consulting companies. The book chronicles evidence-free statements from the most prestigious IT analysis, consulting firms, and enterprise software media. What is clear is that most of the entities that put out articles on enterprise software combine a financial bias with an inability to perform original research — or even to review research that should not have been that difficult to find.

Ubiquity of ERP

Because ERP is now so ubiquitous, it is assumed that ERP is necessary — even if it does not provide any payoff. However, there are a large number of flaws in this common assumption. “ERP” is something. First, it is a concept which is defined by the book as the following:

“Conceptually, ERP is a combined set of modules that share a database and user interface, which supports multiple functions used by different business units.”

However, it is more than this idea, and the following are just some aspects of ERP covered in the book.

- ERP as the Central System: ERP is also a philosophy that ERP should be the center of the IT system – when, in reality, it is simply another application.

- Functionality of Secondary Importance: ERP takes as a foundational assumption that functionality is secondary to integration — which was never confirmed. The benefits of all software — enterprise or consumer — are what the application can do. Integration is a consideration but can never drive what software to purchase. ERP vendors were able to get companies to implement standard functionality that resided in the ERP application and the standard feature in uncompetitive non-ERP solutions that they sold. ERP vendor and their partners — the major consulting companies are significantly responsible for the low efficiency of enterprise software as so much standard and low-functioning software has been implemented by ERP vendors at so many companies.

- ERP as a Method of Account Control: ERP – as practiced by Tier 1 and many Tier 2 vendors, is connected to anti-competitive practices centered around account control. In the grand strategy of the Tier 1 ERP vendors, the ERP system serves as “the wedge.” Once the ERP vendor has sold the ERP system, the ERP vendor has both the established relationships and, from there, uses a variety of logical fallacies to take over as much of the customers’ IT business as possible. The eventual goal is to gobble up as much footprint as possible and to turn the IT department into a passive and controlled entity that implements the software it tells it to.

Including the Larger Picture Analysis — Post ERP Implementation

The studies on ERP ROI are focused only on the ROI of the ERP system. However, none of the studies we reviewed looked at the overall picture. We analyzed this in the Brightwork Solution Architecture Analysis.

The problem with the ROI of just ERP is that it limits the impact of ERP systems on the other purchased applications. This is because of the strategy of ERP vendors to push what are most often marginal applications into the customer by the ERP vendor. A perfect example of this is SAP. SAP has an extremely poor stable of applications outside of their ERP system, the sordid history we covered in the article How SAP is Now Strip Mining its Customers. None of the research includes this very important implication. (Oracle, SAP, Infor, Epicor, Sage), etc…. the more prominent ERP vendors follow this approach.

How Much Do Companies that Implement ERP Know About Their Lack of ROI?

This quotation for Sam Graham, a highly experienced independent ERP consultant, applies.

“ROI rarely comes into the equation. At best, ERP is seen as an inevitable necessary evil, or a ‘rite of passage’ to becoming a big company (SAP had a very effective campaign in the UK (and presumably other markets) a few years back, along the lines of, “Now SAP isn’t just for large companies” which glossed over the fact that they were actually talking about Business One. Clever marketing; and a lot of companies fell for it, believing that they were running the same software as the ‘big boys’.) Rarely do they talk to independent ERP consultants and, when they talk to general management consultants, these people are usually keen to sell their services (and gain experience in ERP) so the last thing that they will do is put obstacles in the way of their clients buying a system.

In my last job in industry, I was taken on as Materials Manager for a $100m t/o Swiss company that had just had a disastrous BPCS implementation. They approached what was then called Coopers & Lybrand (now part of PWC) for assistance. C&L sent in a consultant, who identified more work than one consultant could handle, so they pulled in a second, and then a third. Now; when you had 3 C&L consultants, you had to have a senior consultant to supervise them. And when you had 3 senior consultants, you had to have a partner to manage the 3 senior consultants. So they ended up with a partner, 3 senior consultants and 9 consultants on-site. 5 days a week. I’m not making this up; but it gets worse.

This was in the days of MRPII and, in those days, Ollie Wight & Associates were thought to do the best courses on the subject. So the Partner persuaded our CEO to send all of the company’s management team on a 5-day course. Then, when they came back, he said to the CEO, “You know, now that your people have been on that course, there is a danger that they will use terminology that our people don’t”. So he persuaded the CEO to pay for the same 5-day course for all 13 C&L staff on the project. And that meant not only paying for the courses, hotels, expenses etc; but paying for their time to be on the course!

This is our observation, as well.

Companies that purchase ERP listen to biased entities, ERP vendors, and ERP consulting companies presenting them with sales information.

Why Software Vendors Don’t Want to Know the ROI of Their Software

Considering how often vendors talk about their software having a high ROI, they seem disinterested in calculating it. What explains the vendor’s fear of ROI calculation?

Consulting companies, Gartner, and software vendors frequently state that this or that application has a high ROI. SAP is one of the most common promoters of the great benefits of ROI of their applications. In this article, we will understand how true this is and what vendors want people to know about the ROI on their applications.

The Generalized Assumption of ROI

Software vendors and consulting companies frequently use verbiage such as “improving ROI” for applications that have no evidence of having any ROI. One of the most surprising things is that even the granddaddy of enterprise software, the ERP system, actually does not have evidence of having a positive ROI.

If we look at ERP, what was the evidence that ERP systems had a positive ROI? I analyzed all the academic research on ERP systems and found no evidence of a positive ROI from ERP. I was so surprised by this result after being told the opposite by just about everyone; I wrote a book on these findings called The Real Story Behind ERP: Separating Fiction from Fantasy.

(you can obtain a positive ROI on ERP, but that is a different topic from what usually happens)

The problem, of course, is that vendors and consulting companies have a conflict of interest when describing the ROI of software. Software vendors and consultants are in the business of selling enterprise software. Therefore, there is a natural tendency to underestimate their applications’ costs and overestimate the benefits. A high percentage of software implementations fail to provide any positive ROI, and a high percentage provide a negative ROI. But even with the most significant software implementation failures, the software vendors and consulting companies that perform the implementation still benefit.

And who were the leading proponents of system implementations being a necessary purchase? The software vendors were Deloitte, IBM, Accenture, Gartner, etc. And who were the primary beneficiaries of implementations? Given the shortage of good ROI stories on implementations, the primary beneficiaries, that is, the beneficiaries we can prove are the software vendors, Deloitte, IBM, Accenture, Gartner, etc..

Background on Enterprise Risk Management and Performance Management

One of the most interesting results of evaluating the success metrics applied to enterprise software projects post-go-live is that the only success metrics are related to hitting project management goals — that is, the success metrics are not tied to the system’s actual performance.

“I say “may,” because the research is clear that companies often have no way of validating whether their project was a success because they have no formal measurements in place. The following quotation from research into the project success determination explains this fact – and a fact, which is frequently and easily glossed over when failure statistics are quoted, quite well. “According to Parr and Shanks (2000) “ERP project success simply means bringing the project in on time and on budget.” So, most ERP projects start with a basic management drive to target faster implementation and a more cost-effective project… Summarizing, the project may seem successful if the time/budget constraints have been met, but the system may still be an overall failure or vice versa. So these conventional measures of project success are only partial and possibly misleading measures when taken in isolation (Shenhar and Levy, 1997)” ” – Measures of Success in Project Implementing Enterprise Resource Planning

This quotation is only one example – all of the research in the area of success measurement for IT projects points in the same direction.

How Enterprise Risk Management Relates to the Purchase of Major Enterprise Software and Consulting Brands

Because companies do not measure the success of their projects, they will frequently purchase software and services from major brands. The logic is the following:

“We purchased software from SAP, and we chose our consulting partner as Accenture – therefore what could go wrong.”

It turns out a lot can go wrong. We add a more significant multiple for implementation cost because software implemented by a major consulting company will cost more in every instance we have analyzed and take longer to implement than if no significant software company is involved. This is why the implementation durations of best-of-breed applications are so much faster – major consulting companies do not bring them in. They are not obligated to hand their consulting over to them or to accept the consulting company’s “methodology,” which is not a methodology but a method centered around maximizing the billing hours pulled from the client.

Do Implementing Companies Want Their Projects Evaluated for Success?

The research shows that companies don’t perform enterprise risk management and don’t know if their projects are successful. At first blush, the answer might seem to be “absolutely.” However, do the executives want to find out? If you are an executive at a company and have made a purchase decision, you want the project to be deemed a success. If you measure for success, you may find it is not a success in that the system does not provide the expected output quality and does not improve the company’s condition beyond the system that was replaced. So what do companies do? They essentially measure success based on whether the project met its implementation deadlines. As stated in the Brightwork Research & Analysis Press book Enterprise Software TCO: Calculating and Using Total Cost of Ownership for Decision Making.

It is in fact quite easy to bring up an application so that it is “live.” All that has to be done is client specific master data setup, integration performed to other systems and a generic configuration used. I refer to this as an IT implementation – the system is working and all the server lights are blinking. Implementing the software in a way that adds significant value is the actual goal not simply hitting a deadline. However, in multiple studies it has been found that companies have no other way of objectively determining project success beyond the meeting of project deadlines.

Lets us use an analogy that everyone can relate to. If we look at the wars in Iraq and Afghanistan, were they a success? The bill for these wars is estimated to be roughly $6 trillion.

“The decade-long American wars in Afghanistan and Iraq would end up costing as much as $6 trillion, the equivalent of $75,000 for every American household, calculates the prestigious Harvard University’s Kennedy School of Government.

“The Iraq and Afghanistan conflicts, taken together, will be the most expensive wars in US history—totaling somewhere between $4 trillion and $6 trillion. This includes long-term medical care and disability compensation for service members, veterans and families, military replenishment and social and economic costs. The largest portion of that bill is yet to be paid.”- Global Research

There were great sacrifices on the part of Americans — both in terms of those who funded it and those who fought in these wars. Let us remove from the equation any innocent Iraqis and Afghanis who were injured or killed and the loss of their national independence — or the final impact of these wars on their future. Instead, let us restrict the analysis of the wars as to whether these wars were a success or failure for the US. How does one determine if these wars were a success?

- Is it defeating the militaries of these countries?

- Is it the elimination or reduction of terrorism?

- Is it the possession of these countries’ natural resources?

- Is it the long-term political control of these countries?

- Is it whether both countries begin to operate as great democracies?

There is a strong tendency to declare wars a success because of the sacrifice rather than the benefit; however, for obvious reasons, that can never be a correct measurement. The question that should be asked is not whether sacrifices were made but whether the sacrifices were worth the cost.

Of the $4 to 6 trillion spent, were there other things that could have been done to help the US meet its objectives? As with IT implementations, the output of initiatives seems to be analyzed quite frequently. It also raises the question of, if the analysis is performed and the initiative was a poor investment of resources, does anyone want to know?

How Do You Calculate ROI from Software?

While ROI and improved ROI are thrown around carelessly, the missed consideration is how difficult it is to calculate ROI. Brightwork Research & Analysis has the most extensive and automated total cost of ownership or TCO calculators that exist. Yet, while TCO is difficult enough to calculate, we don’t even bother calculating ROI. The ROI uses the TCO estimate as the starting point; however, how do you estimate the return on a software implementation? There are ways to begin going about it, but it requires too many assumptions. And that is the exciting feature of ROI. The people who make statements about reduced TCO don’t know how complicated calculating is. Before creating our online TCO calculators, we read all the work previously performed on TCO. We found that almost all the entities that calculated TCO had the incentive to underestimate TCO by leaving things out. This is because software vendors perform most TCO calculations.

We then created our own TCO method, which included far more costs than we had seen in any other estimate. Our method is documented in the book Enterprise Software TCO. However, we know that no software vendor even bothered to estimate an all-inclusive TCO, so how can they possibly say they know the ROI of their software? They don’t have any idea.

Conclusion

TCO on ERP is not analyzed outside of academics. Vendors, consulting companies, paid-off IT analysts, and IT media have conveniently circumvented the question of the TCO and ROI of ERP because it leads to all the wrong answers.

Companies that implement ERP systems have not and are not doing the most elementary research to evaluate the potential benefits of the software they purchase. They not only do not research the ROI of the ERP system itself but also do not know the ROI of the follow-up applications that the ERP vendors plan to sell to them after they have captured the account.

Decision-makers don’t measure benefits (measurement is tricky), don’t read academic literature, and benefit by doing things considered “right” at the time. What is considered suitable to be controlled by the marketing departments of vendors and consulting companies that also control the media landscape? So, IoT is being pushed right now. Are there many use cases for IoT? They exist for package delivery and a few other areas, but IoT use cases are quite overstated. Big Data is similarly overstated. However, assertion without evidence is the norm in the IT industry. Loosely translated, the only justifying logic for ERP is that firms that promote ERP propose that ERP is something that should be purchased. That is it. And the firms that recommend ERP most frequently recommend the most expensive ERP systems to implement.